In the first part, we were introduced to the big picture of the existing puzzle pieces in the NFTFi market. In this article, let’s dig deeper into a very potential market niche called Fractionalized NFTs.

What are Fractionalized NFTs?

With the current gloomy market situation, spending large capital to buy NFTs as a hoarding asset is quite risky. Moreover, because of the originality (indivisibility) of tokens of ERC-721 standard, it is difficult for users to invest in NFTs with the DCA strategy. Therefore, a solution to this problem has been found: fractionalized NFTs or fragmented NFTs. This is initially a solution to make it easier for ordinary users to access blue-chip NFTs, which have a very high floor price. Basically, projects provide this solution by converting NFTs into fungible tokens with ERC-20 standard (similar to yield-bearing tokens of DeFi projects like AAVE’s aTokens or SushiSwap’s xTokens).

Fractionalized NFTs projects

Unic.ly and Fractional.art (Tessera)

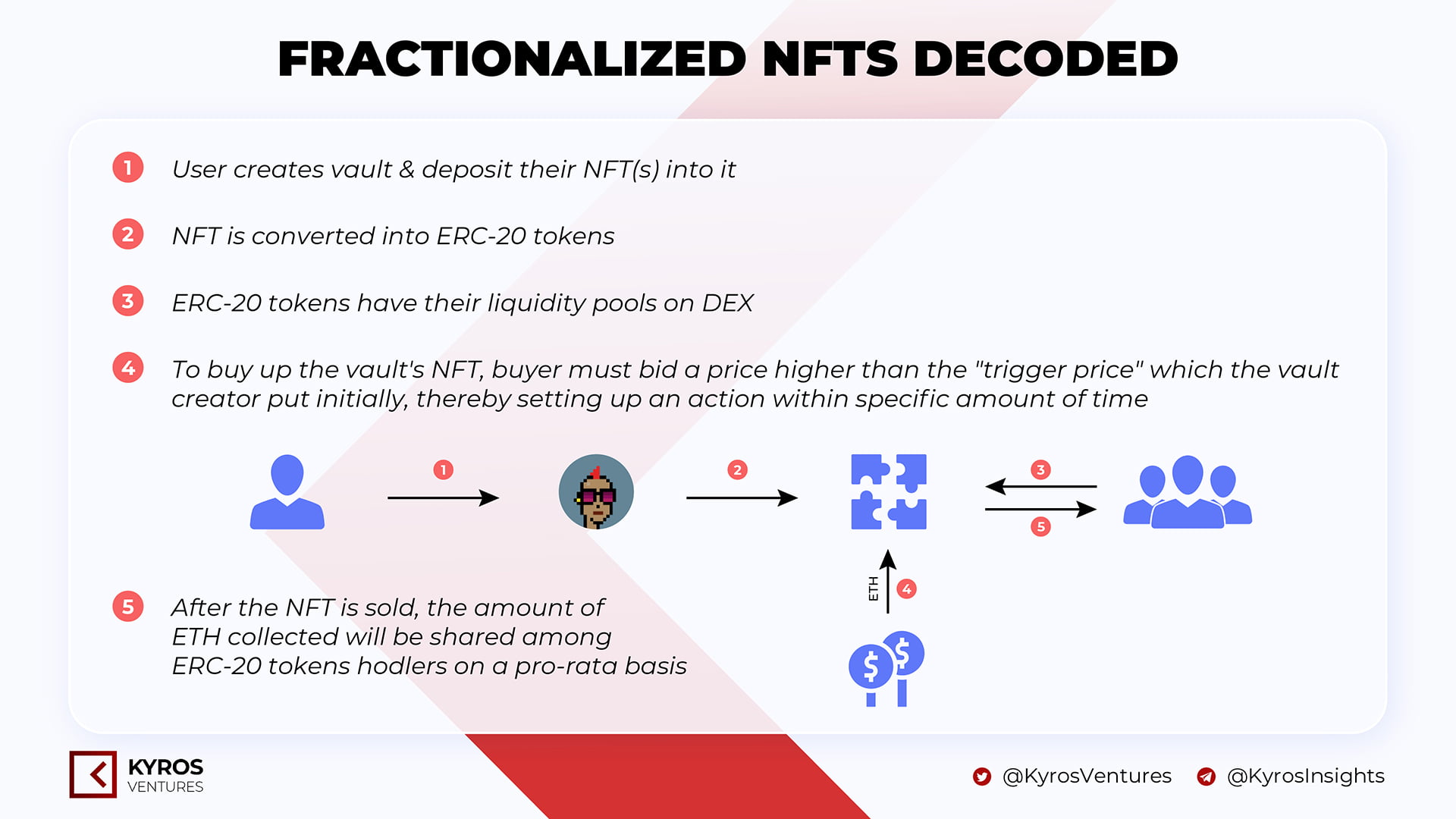

Users can create a vault for one or more NFTs in the same collection and split it into multiple fungible ERC-20 tokens. When another investor wants to redeem an NFT in the Unic.ly vault, they will have to pay a price higher than the trigger price that the vault owner has set. At this point, the auction process will take place, and the overall winner will buy one or more intact NFTs according to ERC-721 or ERC-1155 standards and return the ETH to the vault. The initial investors will be entitled to receive this ETH according to the percentage of their ERC-20 tokens in the vault as shown in Figure 1.

Figure 1. Unic.ly mechanism

Fractional.art has a similar mechanism to Unic.ly, but the trigger price will not be pre-determined by the vault creator. Instead, the co-owners will have to vote to determine the reserve price – the lowest price that the buyer who wants to buy back the original NFT copy has to pay. If more than 50% of the total supply of fragmented NFTs (i.e. ERC-20 tokens) is used for voting, the reserve price will change. This price will be calculated according to the weighted average of all votes.

For example, if 75% vote for a reserve price of 150 ETH and 25% vote for a reserve price of 200 ETH, then the final reserve price result will be 162.5 ETH.

NFT20 and NFTX

These projects also create pools and allow users to deposit NFTs in them like Unic.ly, but the difference is that the buyer has to buy enough ERC-20 tokens in the pool to redeem any NFTs in that pool.

Also, ERC-20 tokens that are fragmented from the original NFTs can stake these tokens for an additional reward of transaction fees (like the LPs of AMMs in DeFi) or mortgage and borrow stablecoins to execute yield farming.

Szns.io

Szns is also a project on NFTs fragmentation, yet with a different approach where the NFTs in each collection acts like the governance token for that collection: Token holders will jointly participate in the process of managing & using the NFTs in the collection through voting.

Bridgesplit

Operating on the Solana blockchain, Bridgesplit has many products around NFTs, typically fractionalization, yield farming with fragmented NFTs, index funds, etc. Like the above projects, Fragmented NFTs can also be traded on Solana AMMs such as Raydium. Token holders will also have voting rights on the selling price and timing of the sale for NFTs.

Assessment

Correlation

The reason that fragmented NFTs are correlated with native NFTs is because of arbitrageurs. For example, when the floor price of CryptoPunks rises, the arbitrageurs will buy ERC-20 tokens in the NFTX pool to obtain an original CryptoPunks, then list that CryptoPunk on OpenSea (which has a floor price higher than the total purchase price of ERC-20 tokens) to make a profit.

Accuracy here can be understood as the correlation of fractionalized tokens with the NFTs they represent in the pool. The higher the correlation coefficient, the more accurately the fractionalized tokens reflect the returns of the original NFTs.

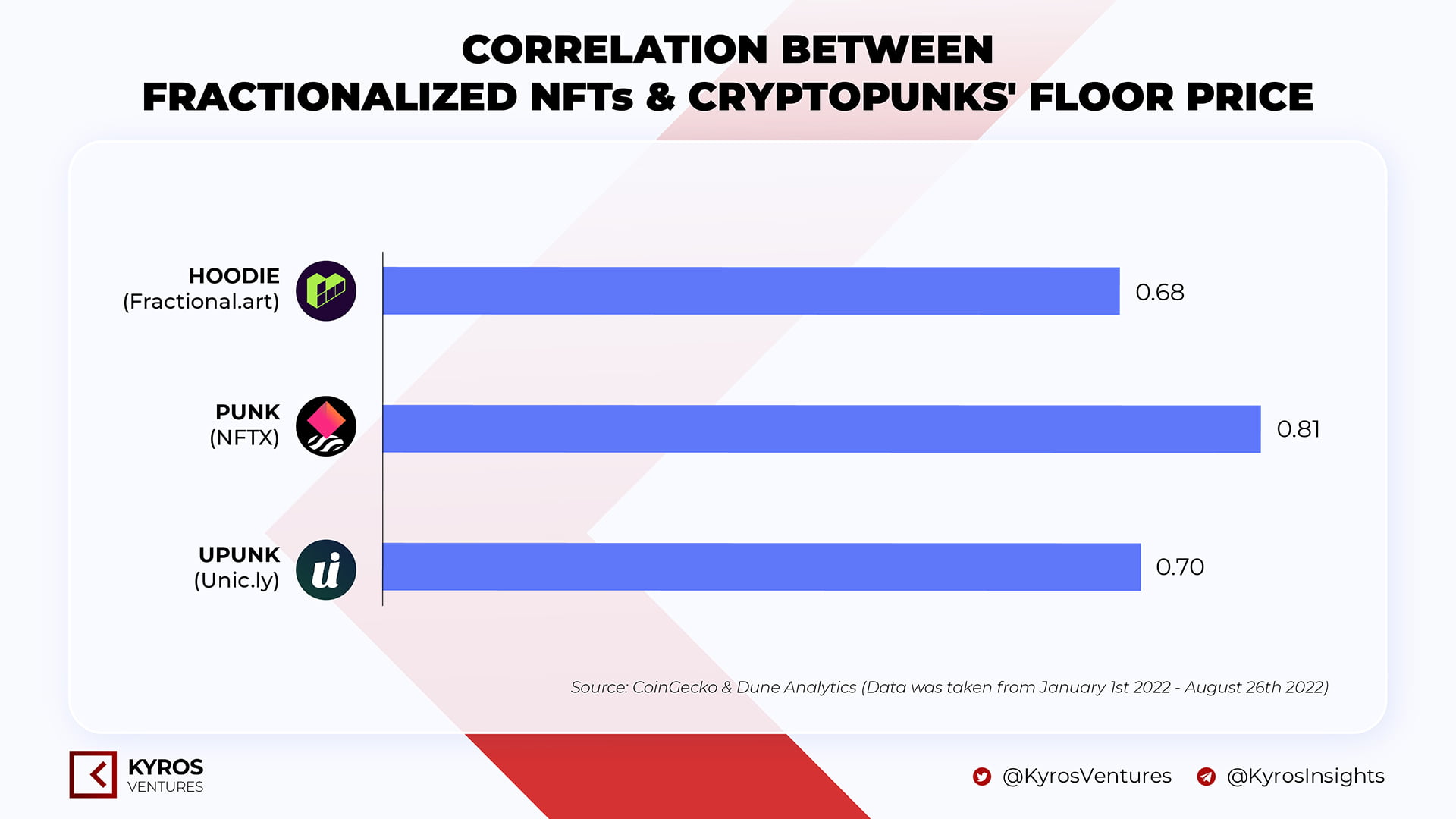

Figure 2. Correlation between Fractionalized NFTs and Native NFTs’ floor price

Figure 2 shows that all fragmented tokens have a positive correlation coefficient (greater than 0) with the floor price of NFT collections. NFTX’s PUNK token shows the most correlation (0.81), followed by Unic.ly’s UPUNK (0.7), Fractional.art’s HOODIE (0.68) and NFT20’s GPUNKS20 (0.54).

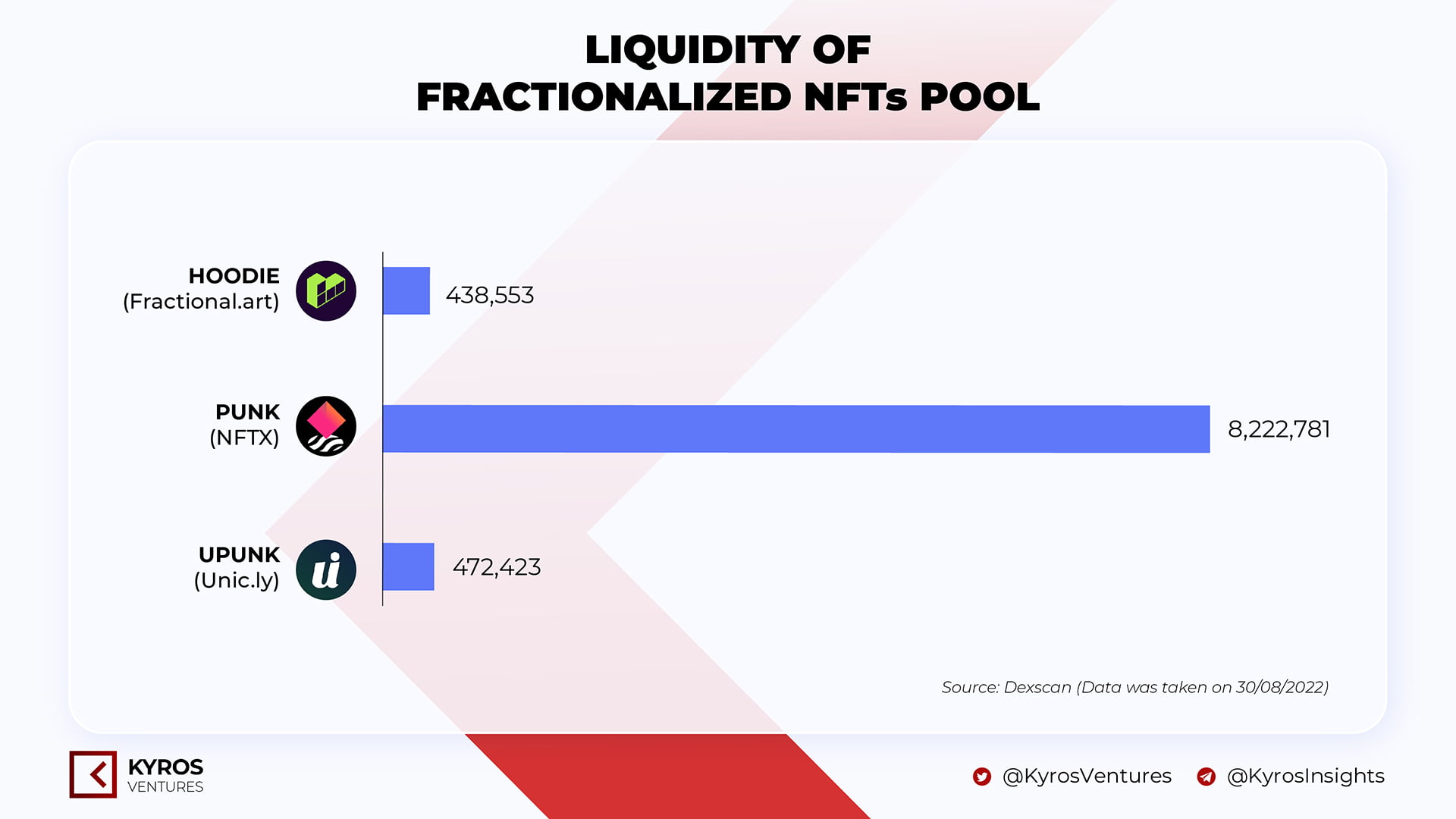

The reason for this difference in correlation is due to the difference in liquidity in the swap pool of fragmented tokens. In particular, PUNK and HOODIE are mainly traded on DEXs while UPUNK is traded on MEXC and Unic.ly’s DEX (Figure 3). Moreover, Fractional.art’s HOODIE token is fragmented from a single NFT, Punk #7171, rather than fragmented from a pool of many NFTs like NFTX, so the liquidity is also somewhat lower.

Figure 3. Liquidity of Fractionalized NFTs pool

SZNS’s MeebitsDAO pool consists of 92 NFTs of which the correlation coefficient to the floor price of BST Meebits is 0.36, and the liquidity in the pool of ERC-20 tokens is around $82,540 (at press time).

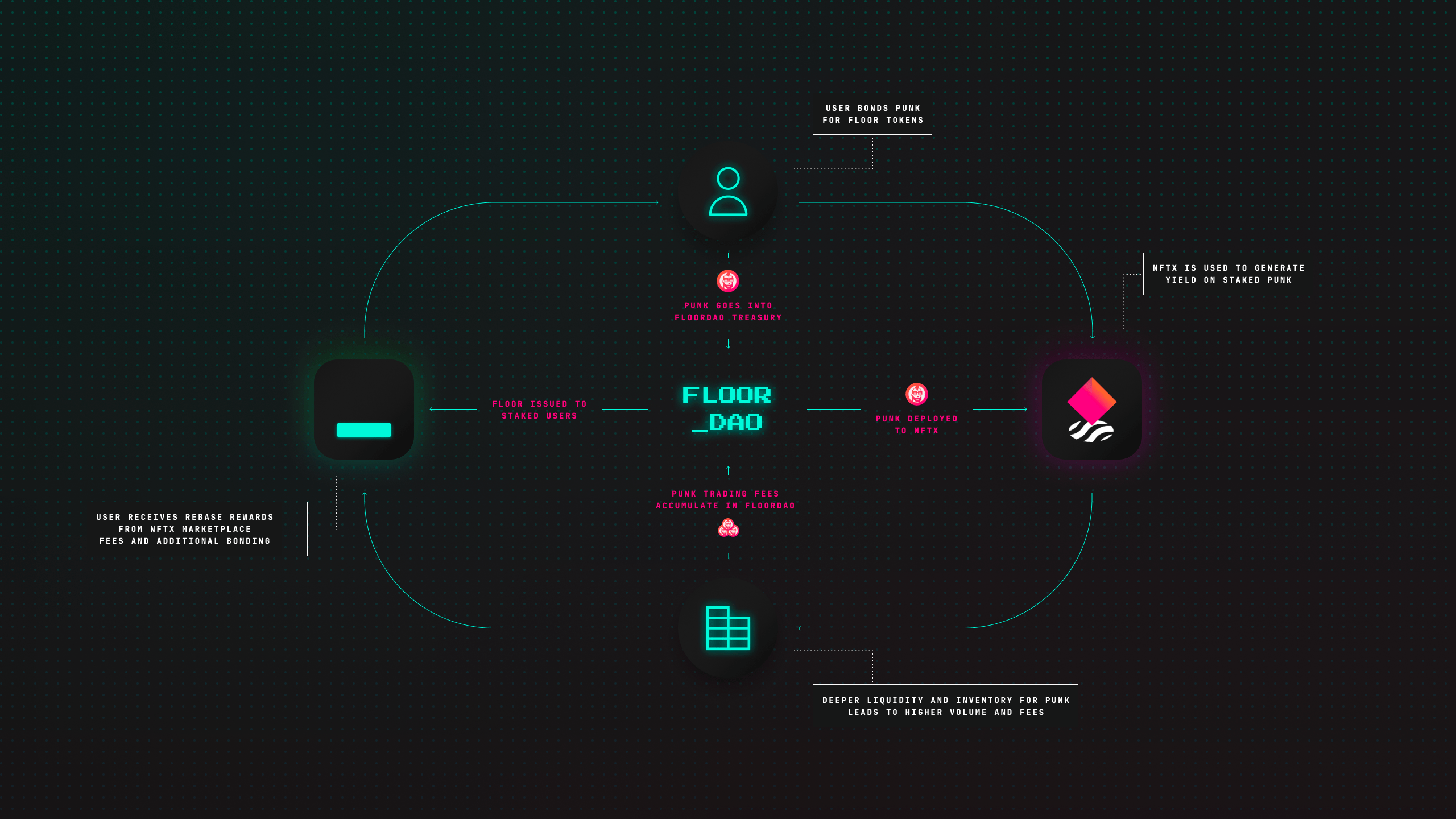

It should also be added, that it is thanks to the high liquidity of the PUNK token that it has been used as a token in the reserve fund of FloorDAO – a protocol that works similar to OlympusDAO (Figure 4):

First, users will deposit PUNK into FloorDAO to receive FLOOR tokens back at a discounted price

FloorDAO will use the PUNK received to continue deploying to NFTX to receive rewards for providing liquidity

Figure 4. FloorDAO mechanism

Ownership

Fragmented NFTs tokens are created mainly to serve investment needs without having to own the NFT. A major downside to holding these fragmented tokens is that users do not have full authority when it comes to buying/selling the fragmented NFTs they hold. Also, NFTs in a normal vault cannot be rented out to create a new cash flow for owners unless the members of the DAO of SZNS organization vote to rent, making the optimization of profit from assets in the pool much reduced.

Epilogue

Fragmented NFTs projects, although not very active, are still a useful tool for investors who want to allocate capital into the NFTs market but are still concerned about the illiquidity of this asset class. Therefore, when investing in the fragmented NFTs segment, investors need to choose reputable projects with high liquidity and active trading volume to minimize risks for their portfolios.

The keyword NFTFi is becoming increasingly popular; will this be the next new trend that combines the best of the two previous trends, DeFi and NFT?

What is NFTFi?

NFTFi, as the name implies, is a combination of NFT and Finance.

The protocols in the NFTFi array were created primarily to increase liquidity for NFTs, an asset class that has previously been considered illiquid due to market volatility as well as their uniqueness – a barrier to price discovery.

Projects in NFTFi will also aid in cash flow optimization for NFT collectors, providing more incentive for them to buy and hoard NFT as an asset class with long-term value rather than a means of speculative facilities as it is now.

Basically, NFTFi projects convert NFTs into fungible tokens with ERC-20 standard, similar to yield-bearing tokens of DeFi projects like AAVE’s aTokens or SushiSwap’s xTokens.

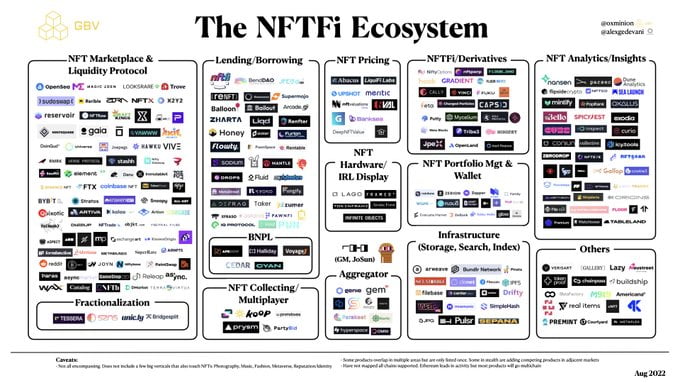

NFTFi ecosystem (Source: 0xMinion at GBV)

Main sections in NFTFi

Provide liquidity

The Marketplace model – NFT floor – is the most popular today because it connects NFT buyers and sellers and serves as a source of liquidity for the entire market. The price formation process is based on the bid and ask prices that are arbitrarily set between two parties.

Ecosystem

Notable NFT exchanges

Ethereum

OpenSea, LooksRare

Solana

Magic Eden

Polygon

OpenSea

Flow

Flowverse

Avalanche

Joepegs, NFTrade, Chikn

However, as a result of the aforementioned bid-ask mechanism, NFT has become a less liquid asset than other investment channels such as stocks or cryptocurrencies because NFTs in the same collection are sold at a low price. The rarity or attractiveness of some of their characteristics determines their value. The use of various valuation methods, including emotional pricing, has widened the spread between the bid and ask prices for most NFTs on the market today.

Several liquidity solutions were developed to solve this problem, most notably fractionalized NFT (fragmented NFT) and AMM (Automated Market Maker).

Fractionalization is a solution that allows ordinary users to access blue-chip NFT collections, which have a very high floor price – potentially ranging from a few tens to millions of dollars. Some protocols, such as Unic.ly or Fractional.art, provide this solution by converting NFTs into fungible tokens compliant with ERC-20 standards (similar to yield-bearing tokens from DeFi projects such as AAVE’s aToken or SushiSwap’s xToken). Through speculators specializing in arbitrage, the price of these ERC-20 tokens will move according to the floor price of collections on the traditional NFT market, allowing users to profit when investing in a highly volatile asset like NFT but without the huge risk of putting up a large amount of capital at an early stage.

AMM is also a solution born to solve NFT’s liquidity problem. Still, it targets the disadvantage of the bid-ask mechanism when buying and selling NFT on traditional exchanges by allowing users to buy/sell NFT via instant liquidity pools. For example, one of the recent AMM for NFT projects is sudoswap/sudoAMM. If the formula x*y = k is applied to the valuation of pool assets like DeFi’s AMMs, slippage will be high because NFTs are inherently indivisible, unlike ERC-20 tokens. Therefore, the sudoswap project has applied the bonding curve model to determine the price increase/decrease every time an NFT in the pool is bought/sold to ETH.

Credit

Credit segment projects are divided into two types: Lending and pre-paid post-purchases (BNPL).

Lending in NFT works similarly to DeFi, except the collateral is NFTs (usually blue-chip NFTs because they are more liquid) rather than ERC-20 tokens. To protect lenders, the project may devise a formula for calculating an appropriate liquidation price threshold when the floor price of the NFT collection begins to fall. Some projects, such as JPEG’d, also allow NFT collateral to be used to mint stablecoins, using a mechanism similar to the Collateral debt positions (CDPs) used for MakerDAO’s DAI.

For BNPL projects, the buyer must place a down payment in order to receive or gain access to some of the NFT’s existing benefits, and the balance must be paid back within a short period of time (depending on the project’s regulations). This service is supported by platforms such as Cyan, ApeNow, and BendDAO.

Valuation Tool

Valuation is critical for NFT investors because the current state of speculation and flash inflation makes it difficult for them to make independent investment decisions.

Most NFT pricing platforms today use AI technology, such as NFTvaluations or Upshot, while others use crowd-sourcing price formation such as Abascus and PawnHouse.

Derivatives

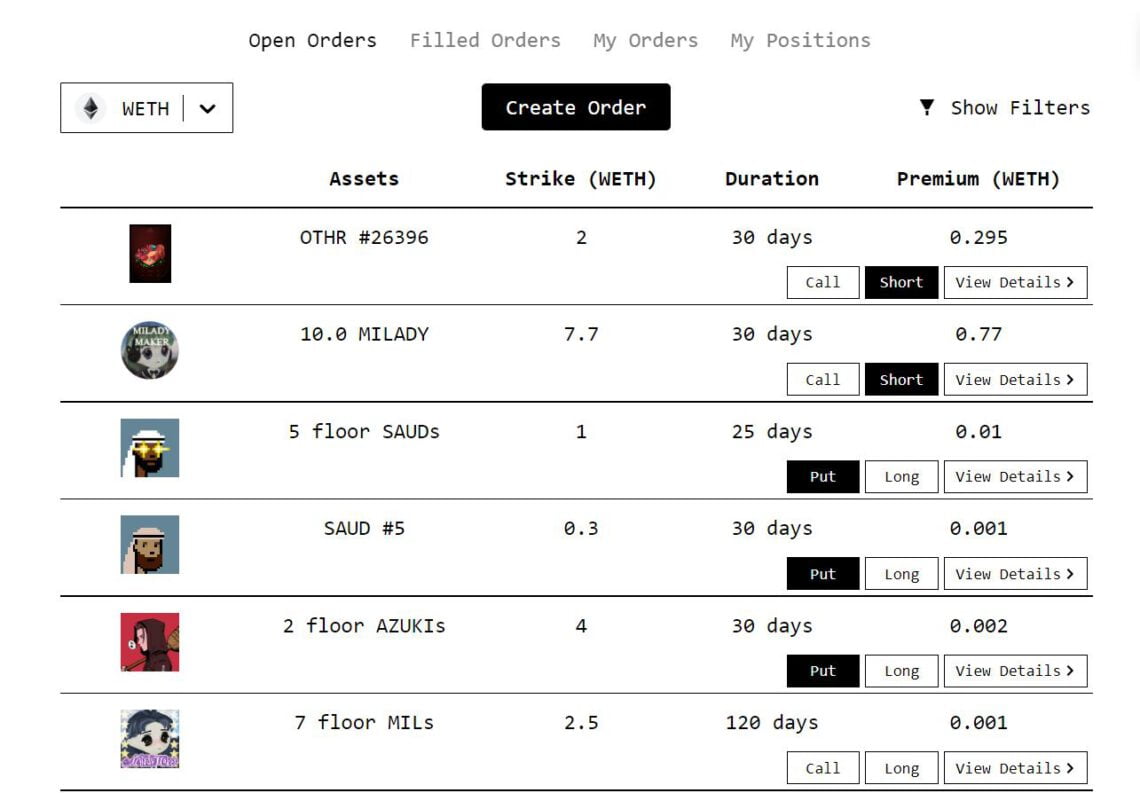

NFT derivatives platforms function similarly to DeFi derivatives platforms. Users can buy and sell options contracts to hedge risk or optimize cash flow from their assets, depending on their investment strategy and market forecast.

Call/put options of various NFT collections listed on Putty.finance

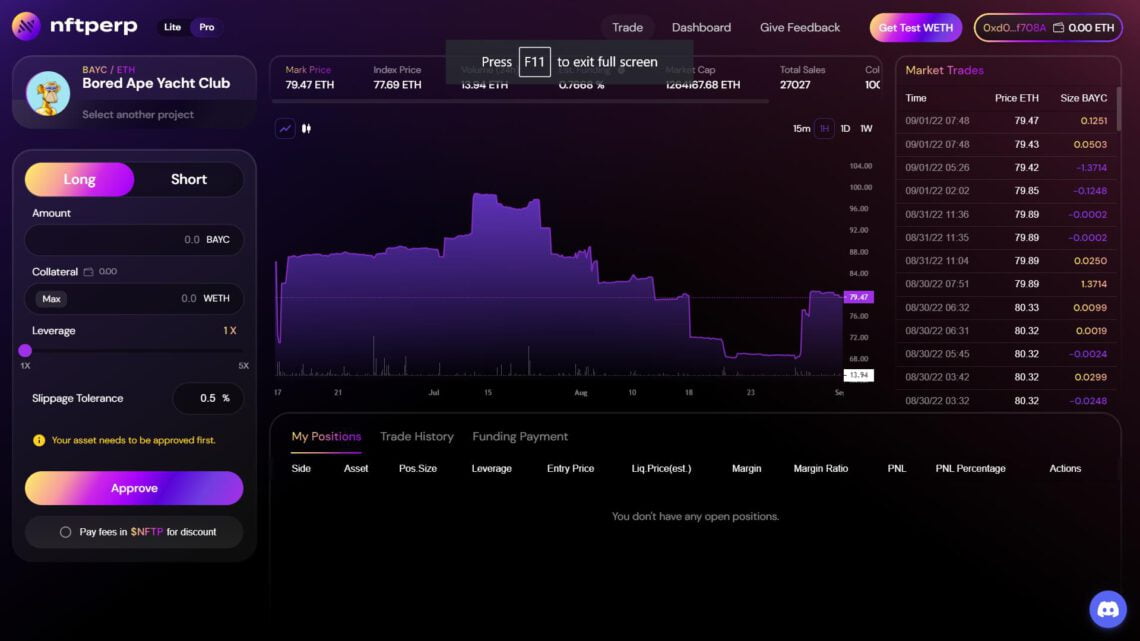

The majority of NFT’s derivative projects are starting to take shape, demo, or launch. Among these are nftperp, Mimicry (the NFT prediction market), and Hook (which is in the testing phase on the testnet).

Demo version of NFT perpetual contract

Liquidity Aggregator

An aggregator is a solution that aggregates prices from various NFT exchanges in order to provide users with an “all-in-one” data source when purchasing or selling NFTs. Gem.xyz (acquired by OpenSea) and Genie (acquired by Uniswap) are two prominent platforms in this segment. According to Dune Analytics data, even though the number of transactions on these two platforms has decreased significantly since the beginning of June 2022, Gem continues to outperform and outnumber its competitors. While on Solana, Hyperspace is the popular NFT liquidity aggregator.

;

Epilogue

As mentioned above, NFTFi projects have not received much attention yet and are still in the finishing stage. Therefore, the explosion of NFTFi until now is still a big unknown to many people.

In the following parts of this series, each piece of the NFTFi puzzle will be dissected and analyzed so that you can have more precise judgments about the potential of NFTFi in the near future.

Sudoswap has just announced the preparation of an airdrop of SUDO tokens for users. Is this the first light of the NFTFi summer day?

Like traditional identity documents (IDs), wallets have always been our gateway to the crypto world. This article is about the Web3 cryptocurrency wallet and its differences from Web2 e-wallets like ApplePay or PayPal we used to know. In essence, the Web3 wallet also serves the purpose of storage and transactions like e-wallets in Web2. However, it improves the operating model, allowing users more freedom and security.

Web3 wallet landscape

The whole e-payments market is expected to reach 4.8 billion by 2025. Payment/wallet businesses have enjoyed revenue growth, especially since more and more applications are continually integrating with online payment.

The number of investments poured into the Web3 wallet applications is approximately $3.3 billion. Recently, the leading web3 wallet company ConsenSys – Metamask raised $450M, bringing the company’s valuation to $7 billion. As more new ecosystems are launched, the number of wallet addresses increases significantly because no one wants to miss this “dreamland”. At the same time, the expansion of ecosystems leading to the primary development trend of Web3 wallet projects today is to deploy multi-chain wallets (Figure 1).

Figure 1. Web3 wallet landscape

Operating model

The blockchain wallet can be interpreted as an interface for users to interact with the blockchain. Its primary function is to store assets or perform transactions.

Blockchain wallets are divided into two types: custodial and non-custodial. We can also classify this according to the connection of the wallet: cold wallet (offline) and hot wallet (online).

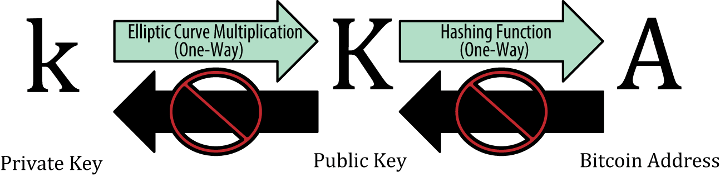

Each wallet will include a public key & a private key: When a user creates a new “account”, an encryption algorithm will generate a private key; From the private key, generate a public key; From the public key, and generate a wallet address.

Note that this path only goes in one direction; there is no reverse (ie, no one can know the private key even if they know the wallet address).

The private key works like a unique key to open your safe because every transaction on an account requires the signature of the private key.

Figure 2. How does a Bitcoin wallet work (Source: Blocktrade)

The only difference between custodial and non-custodial wallets is who manages the private key. Like its name, non-custodial wallets require the user to keep and manage the private key themselves, while in custodial wallets, the private key will be stored by a third party.

Key storage

Commonly used methods to store secret keys:

Store on hardware: this storage method is considered the safest, but they are also less convenient than the above storage methods.

Local key storage: The key is stored on the device and can be accessed from software that points to a specific location in a database. Although convenient and fast, this method is not secure and vulnerable to attacks.

Store with password (password-protected key): This method is similar to the above, but there will be an extra layer of security in the middle – only when the user enters the correct password then be able to access the private key. However, hackers can still steal passwords through spyware that tracks keystrokes or through brute force (a trial-error process on the computer to find the end result).

Password-driven key: The password will be used as a control directly from the public-secret key pair. However, hackers can still attack this method by using random passwords to find these public-private key pairs (i.e. from the password “iloveyou” will find a corresponding key pair). Therefore, hackers can easily trace the private-public key pair of a user’s wallet address if he/she sets a weak password.

Model shifting

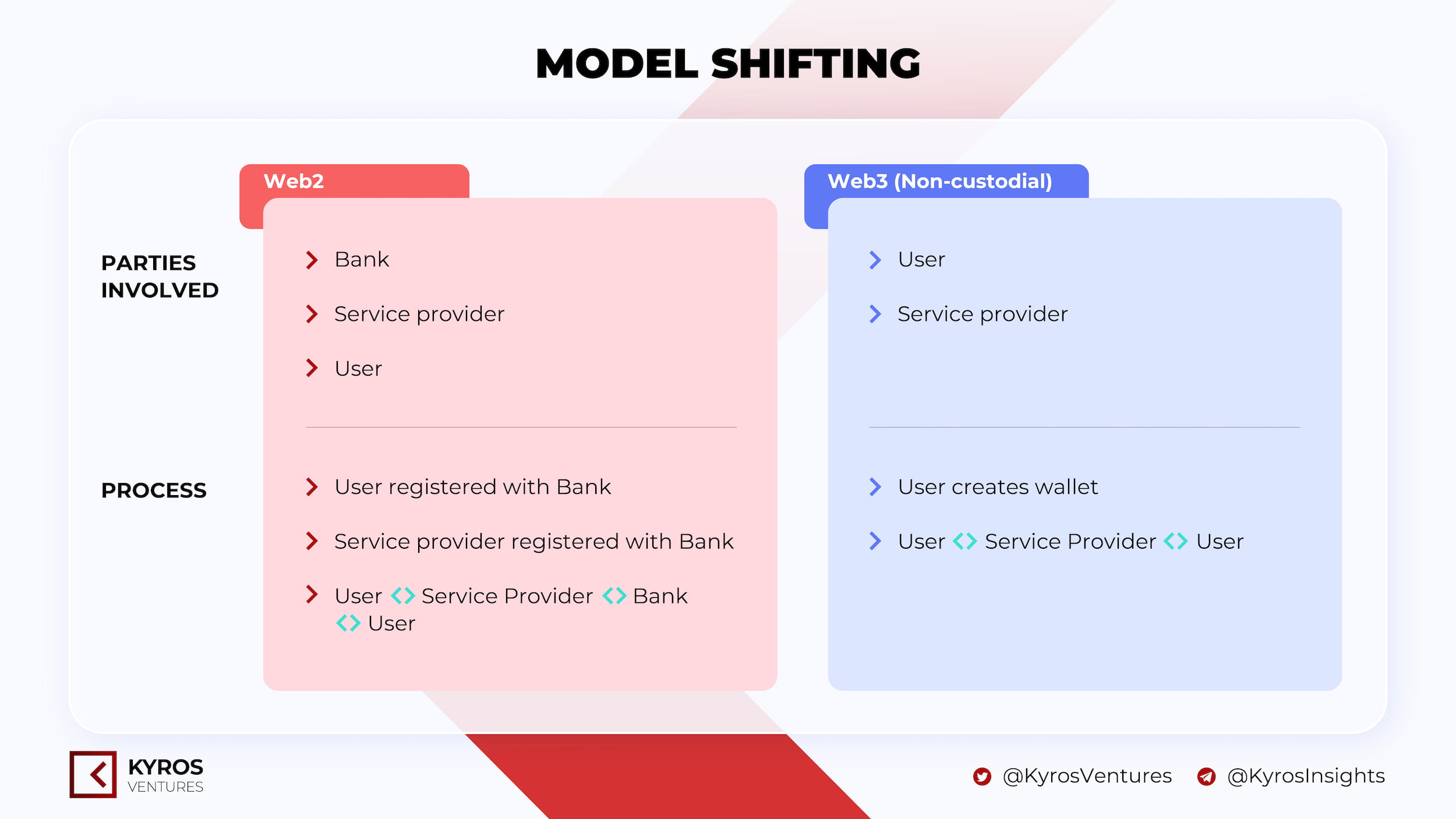

The model of e-wallets in Web2 involved three parties: User, Bank, and Service provider. Users need the participation of 3rd parties such as banks to store and confirm transactions and service providers to perform payments and connect between banks and senders/receivers.

A custody crypto wallet is a service provided by a centralized exchange like Binance and Coinbase. The service is to support you in keeping your wallet signature, meaning that they can keep and manage your private keys on your behalf. In other words, you won’t have full control of your funds nor the ability to sign transactions, which is similar to the e-wallet at Web2.

In contrast, with the non-custodial wallet model, users do not need to worry about intermediaries like banks because they have complete control over their wallets and assets. Because of cutting intermediaries, users do not need to go through the complicated authentication process steps or share personal information (Figure 3).

Figure 3. E-wallet model shifting

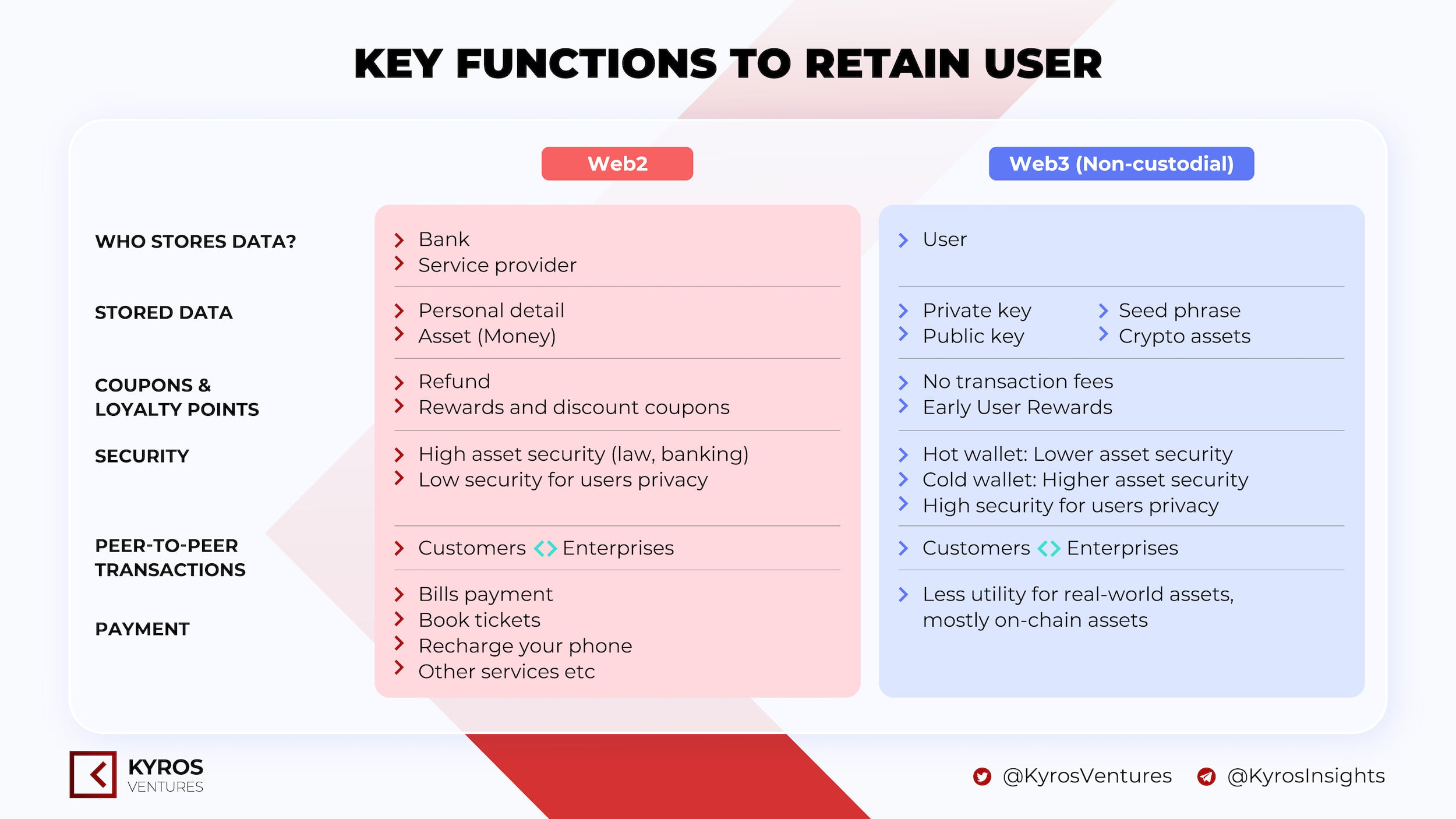

Key functions to retain user

Figure 4: Key functions to retain user

The Web3 custodial wallet model has similar characteristics to the Web2 e-wallet, so it is suitable for less experienced users who need 3rd party support. Custody wallets such as Binance Custody are compliant and provide standard coverage for Binance accounts. Therefore, providing more legal security for the user in exchange for the user’s personal data (KYC).

On the other hand, privacy protection is one of the most prominent features of Web3 non-custodial wallets (Figure 4). User personal data is safe and secure when it no longer needs to be provided to any 3rd party. Thus, it is possible to prevent the relevant leaking information actors.

In terms of security, hardware wallets have the highest safety, suitable for users for long-term investment and storage. Hardware wallets are not directly connected to the internet, thus ensuring a high level of security for large sums. Hot wallets are less secure and more vulnerable to attacks because they are stored and frequently interact over the internet. Recently, we saw a leak of users’ private keys from the Slope wallet platform, with a total loss of up to 6 million USD for users.

To solve the aforementioned security issues, Vitalik has come up with a solution called social recovery wallet. They combine the ease-of-use of single-signature wallet with the better security property of multi-signature wallet by adding a group of guardians: in case everything runs smoothly, users still use the social recovery wallet as the normal single-signature wallet, but in the case of being hacked, the wallet’s owner can send a request to the guardians group to change the current signing key of the hacked wallet to a new one of the owner (but they must wait 1-3 days to execute this). Nevertheless, the current infrastructure of Ethereum does not allow for direct implementation of social recovery wallet but a third-party relayer who will be responsible for re-submitting signed messages as transactions to the blockchain, adding up the transaction fees as well as the centralization of the protocols.

In terms of payment application coverage, Web2 wallets can pay for almost anything, especially in countries with mature financial infrastructure. Whereas Web3 has less utility for real-world assets, payments are primarily made to on-chain purchases. However, there have been more positive signs as more brands and products accept crypto payments, opening the door to growth for Web3 wallets.

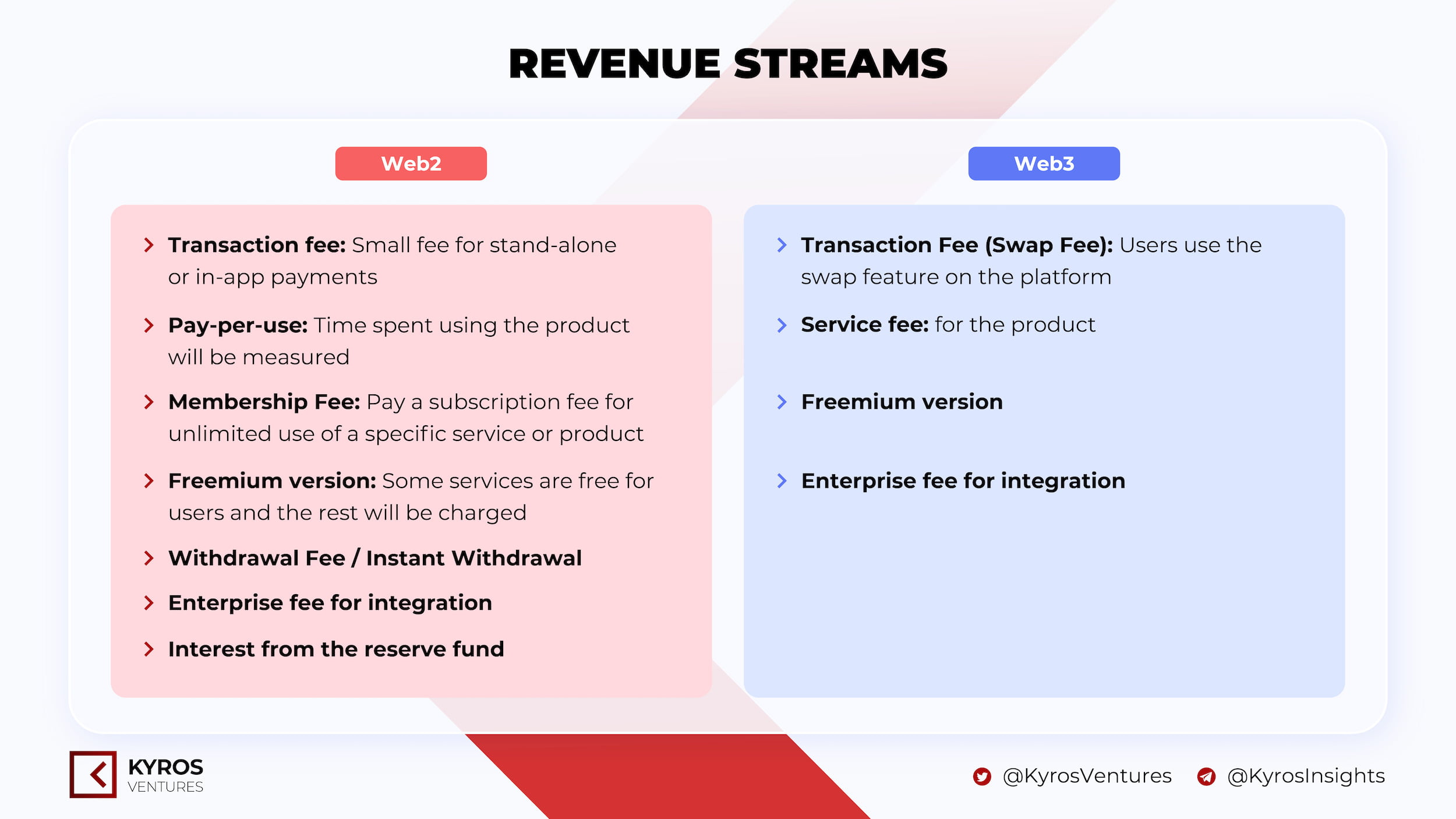

Revenue streams

Figure 5: Revenue streams of Web3 wallet

Some examples for web3 wallet revenue models:

Transaction fee:

Metamasks charges transaction fee from 0.3% – 0.875%.

Phantom charges a 0.85% fee for all transactions.

Enterprise fees for integration: MetaMask offers MetaMask Institutions (MMI), an “institutional extension” of the MetaMask wallet specifically designed for funds speculators, crypto funds, financial institutions, market makers, etc.

Freemium version: Trust Wallet is free for users. All fees are paid to miners or validators. In addition, Trust Wallet also launched the $TWT token to control its own economy.

In general, Web3 wallets are heading towards building many different features aimed at acquiring and retaining users. Meanwhile, the main and most sustainable source of income is still transaction fees. Thus, we can view the Web3 wallet model as a variant of DEX that focuses more on payment and transaction utilities than DEX.

Some highlights

In Web2, the number of e-wallets is up to 2.8 billion wallets. Meanwhile, Web3 only reached about 300+ million wallet addresses. Obviously, Web3 has much room to expand further to reach the number of users who have used e-wallets in the past.

In addition, Web3 wallet applications witnessed impressive growth in 2021: Metamask is up 1800% and blockchain.com is up 72%. A large part of the growth in the number of Web3 wallet addresses is due to the GameFi/NFT boom in 2021.

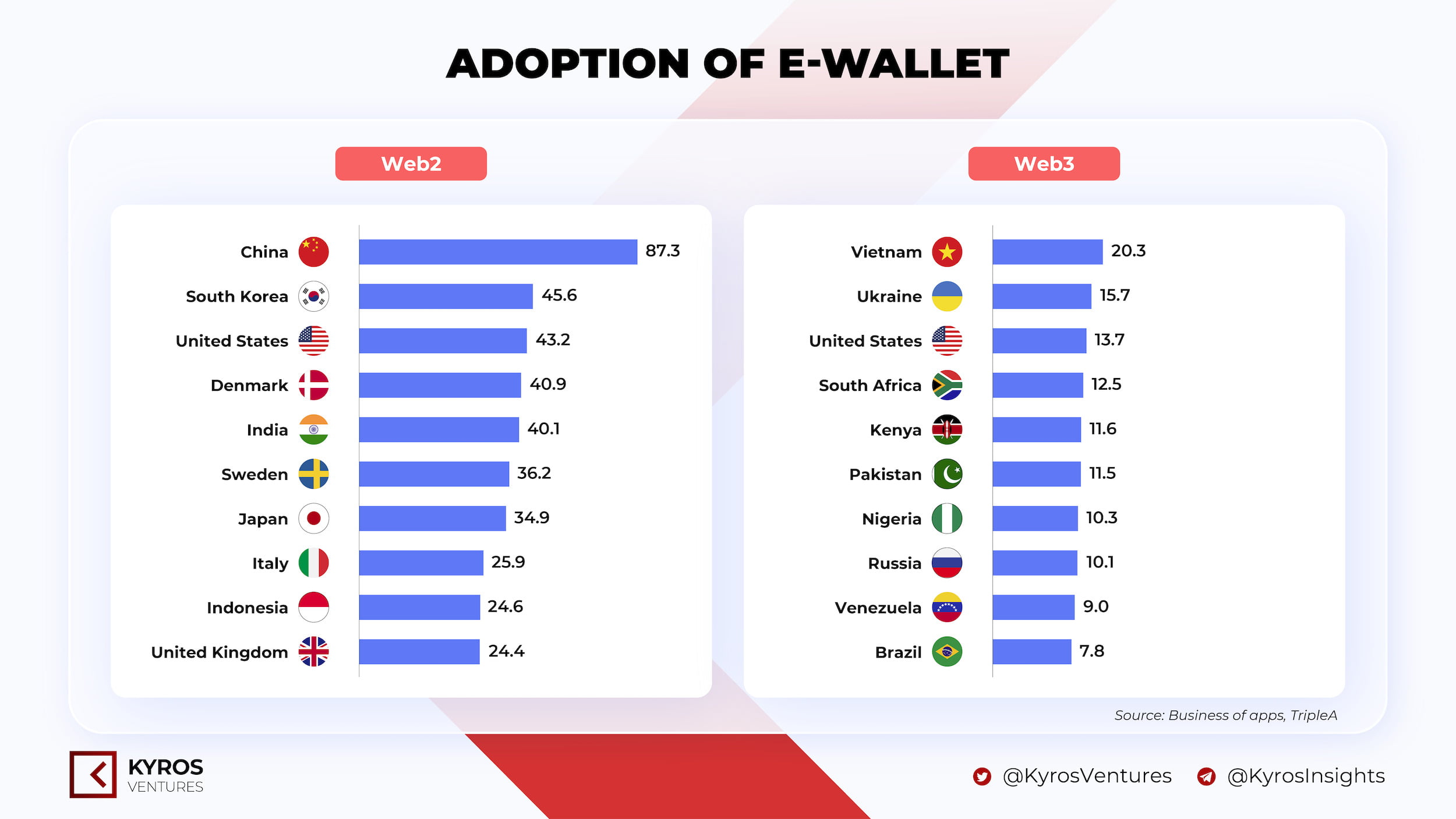

Adoption of e-wallet

Southeast Asia and the Middle East will continue leading the growth of Web3 wallets due to their limitations with banking and credit cards. In other words, because of lacking financial instruments, the chance for web3 wallets to develop in these regions is higher than in countries with fully established financial systems. One example is the rise of the Axie Infinity game, which has brought a new inflow of users into the cryptocurrency market. Most participants are in developing countries, and Axie opens up new financial opportunities for users in these regions.

Slow growth in Western Europe, North America and China, as these are not crypto-friendly countries. These regions have a complete financial infrastructure, providing a variety of online financial services to the people. In particular, crypto creates problems with illegal money transfers and destabilizes the financial systems of these countries.

What’s under development

Integration: MetaMask launched Snaps earlier this year, a system that allows developers to extend and customize MetaMask wallet features in a different coding environment. Users are free to experiment with these new features, and the MetaMask team will consider integrating the most popular feature into their final product.

Multi-chain: This is an inevitable trend that almost all wallets aim for. The shift to multi-chain helps users conveniently transact between different chains on a single wallet interface. It also helps them better manage their assets by only having to store one private key/seed phrase instead of many complex private keys for different chains.

Simplify UX: Many new features have been launched to help users directly buy/sell/list coins or NFTs in the wallet. It even cooperates with CEX exchanges to shorten the time of transferring tokens between non-custodial wallets and CEX exchanges.

Native swap

Roses are red🌹

Violets are blue

But first, let’s check

What Native Swap brings to you?

No more manually checking on multiple AMMs to find the best prices. Just select Blockchain & proceed with your transaction right away🚀

— Coin98 Super App (Formerly Coin98 Wallet) (@coin98_wallet) August 4, 2022

Direct listing

Listing NFTs on @MagicEden from Phantom is available to everyone on all devices! Did you know that you can also use your wallet to edit prices and remove listings?

It’s super convenient from our mobile apps when you (or floor prices) are on the move!! 🧹🧹 pic.twitter.com/OeLIrKYlIG

Social recovery wallet: social wallet brings more convenience for users to get their assets back if they lose or get hacked into their wallets. The confusing numbers of private key or mnemonic passphrases will no longer be a big obstacle for users.

New revenue models: The revenue generation models of Web3 wallets were “imported” from Web2, but there has not been much improvement in adding revenue. The revenue from transaction fees still contributes to the bottom line in bringing profit for both the e-wallets in Web2 and Web3. In the future, Web3 wallets will need to introduce new features, not swaps, stakes, or yield farms but also products that provide data to help users with their better investment strategies. Additional services such as insurance, in-app shopping, consulting, etc., in Web2 can be extended to Web3 wallets. Although these services cannot replace the primary source of revenue from transaction fees, it will diversify products to attract and retain users.

Let’s be honest here. Web3, Web4,… Webn 🧐 I don’t think that you care, neither do I. We are here for the Music, it’s all that matter! “Will/how the changes impact us as a fan or an artist” is a different story and maybe it doesn’t even matter to listeners.

If you are curious, let’s dive in!

Just a short brief

(i) Art + NFT, Game + NFT and now Music + NFT

What was the last time you opened music from a cassette or DVD?

You may not probably recall. That’s the beauty when technology meets music. It comes with the promise of giving artists more chances to thrive and giving users a better experience with music, not just listening but also engagement.

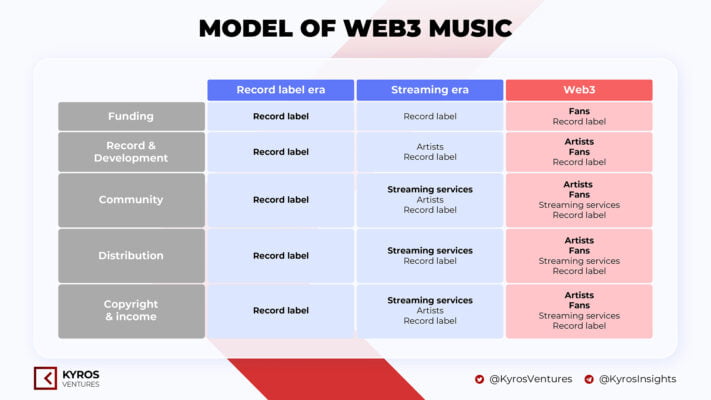

The rise of NFT in 2021 has seen the birth of a new model in the music industry, altering the power position of the parties that keep the wheel running in Web2: Publishers and Record labels to the hands of artists and fans.

(ii) Artists don’t get paid as they deserve

In the current system, artists only receive about 12% of the royalty fees for their products, and most of it goes to the pockets of major record labels or music streaming platforms (Spotify, Apple Music, etc.). Meanwhile, artists at Web3 can earn 100% of their profits from selling their NFTs. In addition, artists also receive a royalty fee, determined by artists, for every time users trade NFT.

Problems there. Worth changing if Web3 can.

Digging into the current problems of Web2 music

(i) Power has never been in the hands of artists or fan

Before the internet era, Record Labels is the third wheel of the relationship between fans and artists

In the 60s and 70s, musicians needed to be contracted by record labels for song rights. Therefore, record labels monopolize the entire industry because they have money, own production studios and provide distribution channels. Those are things that are luxuries for artists these days. Thus, royalties for recordings by musicians are the price in exchange for these services. Monopoly always comes with the hand of power and manipulation. At this time, artists and fans are both depended on the Record labels.

⚠️ Artists → Record labels → Fan

After the internet came, Publishers replaced Record labels to become the next third wheel

Since the 2000s, the popularity of desktop computers and MP3s have opened new doors for artists as they can now compose at home and distribute on the Internet. With the opening of the streaming industry, many distribution service platforms like Spotify, YouTube, etc., have become alternatives for Record labels. Record labels since then have lost their exclusive privileges to production and distribution.

But again, power and manipulation don’t just disappear; it just transfers from one to another. Now, the primary control between artists and fans is the music streaming platforms.

⚠️ Artists → Publishers → Fan

(ii) Artists’ loss of ownership, a higher requirement for entry and a lower income

Fundraising: Record labels dominate the fundraising market, artists have nowhere to go.

Though with the development of technology allowing artists to be independent in producing music, in 2021, Record labels still account for 70.1% of the market share of the entire music industry compared to independent artists, so-called indie artists. The record labels remain the key player capable of providing artists with resources to produce music.

Ownership: Copyrights mostly belong to record labels and streaming platforms.

Before the Internet era, the Record labels monopolized the supply chain for the music industry, dominating the production and distribution of music products in the market. As the Internet became more popular, the Record labels’ monopoly in distribution was replaced by music streaming platforms. However, as mentioned above, the Record labels are still crucial in the production stage.

Artists depend on third parties in both the production and distribution phases. Thus, they need to share music copyrights with Record labels or Streaming platforms.

Income: artist’s income is dominated by Record labels and Web2 streaming platforms.

When artists lose a lot of copyrights to Record labels and streaming platforms, their share is as low as 12% royalties from their music.

Next, 33% of all new Spotify artists discovered happens on playlists personalized by Spotify for users. “Personalized for users” is a fancy word, but it’s actually Spotify’s playlists. Like other social media platforms, they navigate what we listen and what they want us to listen. Control from streaming platforms has become a significant barrier for artists as the review and selection processes become more challenging on those platforms. Because, as you know, that’s their golden egg for maximizing profits.

Web3 and its better offers to take over Web2 music

(i) Power back in hands of artists and fan

Web3 cut off all third wheels, Fans and Artists are closer than ever

Finally, we see the association between artists and fans have changed into a two-way relationship. Now, fans can directly contribute to the artist’s success with NFT through activities such as fundraising, voting on the development of the campaign, and more.

💡 Artist ↔ Fan

Model artist-direct-to-fan works in traditional music before

Neil Young, who has turned his back on Spotify and built his own streaming platform, earned himself 25,000 subscription fans with a total of $600,000 in membership fees yearly.

Another artist is Melissa Etheridge, who launched her own subscription platform and earned over $500,000 annually.

(ii) Artists take back ownership, entry as will and earn more income

Fundraising: No need for record labels, artists have fans

With the innovation of Web3 technology, the music industry model has shifted power from intermediaries to musicians and fans. Music NFT becomes a tool for artists to raise capital and distribute directly to their fans. Conversely, the fans themselves can become a “self-record label” for the artist by investing in that artist’s music products and receiving a portion of their copyrights in return.

Ownership: Third wheels have gone, copyrights are back in the hands of artists (and fans as will)

Artists can now raise money through fans without needing Record labels; artists can also distribute their own music on Web3 streaming platforms without needing a Publisher on Web2. And guess what? When they no longer depend on any intermediary to bring their work to the audience, the artist has full ownership and control over the work’s copyright.

Income: No more domination means a higher income

Web3 allows fans to invest in an artist’s NFT, unlocking many other income sources for artists. For example, Alan Walker collaborated with Web3 artist fundraising platform Corite to launch his NFT collection called Alan Walker Origins. In particular, users need to own 25 NFTs corresponding to the pieces of music to combine into one perfect song. The Alan Walker Origins campaign raised $355,380 for the artist. Besides allowing the artist to raise funds from the fan community, the artist can also receive a portion of the fee from each NFT transaction.

In 2021 alone, NFT has helped big-name artists raise millions of dollars in sales. Of which 3LAU earned $11.7 million for the Ultraviolet collection, Steve Aoki took in $5.8 million from the WarNymph Collection, Vol. 1 and $4.25 million for the Dream Catcher.

The new model of Web3 Music

Record labels will continue to fall further in their position with the artist. With tools and platforms like Corite and Audius, NFT enables a more direct and independent way of funding and go-to-market through Music NFT sales. By empowering fans to directly become individuals/communities to perform Publishers tasks like marketing, music distribution, or even joining the artists’ development plan for their creation and campaign, fans minimize Publishers’ power over artists’ success. These new and exciting tools allow artists to increase the value of their work while maintaining ownership of their music.

What I found challenging for Web3 Music

(i) New tech and highly independent may not be for everyone

Considering that being an artist is a profession, the ‘direct to the fan’ approach is not something that works for every artist. Daniel Allan is a case that prefers to go for third parties rather than do-it-himself in Web3. More independence in creative power, more ownership, and potentially higher income are undeniable benefits of Web3, but that’s in exchange for a much larger workload.

While third parties may no longer be the sole gatekeepers in production and distribution, their value lies in experience, resources, and connections for achieving large-scale success in the music industry.

In addition, most artists who’ve successfully raised a handful of money in Web3 are well-known artists in the tradition. At the same time, the target audience for Web3 is new and for unknown artists, it is tough for them to do everything by themselves. As mentioned above, 1/3 of new artists are discovered through the suggestions of streaming platforms. Some artists are better trying their luck on Web2 instead of Web3 streaming platforms with a limited number of users.

(ii) Things don’t change overnight, major income for artists’ products still comes from Web2 streaming

There are many alternative ways for artists to make money on Web3. However, their music products’ primary income source still comes mainly from major Streaming platforms such as Spotify, Apple Music, etc. In Web3 royalty platforms such as Corite or Audius, the artist can share revenue with NFT owners through the streaming revenue on Web2 Streaming platforms. As noted above, it doesn’t bring many benefits for users especially when Web2 media are still dominating the supply.

(iii) It’s still a new technology, hacks and exploits are inevitable

The hack happened to the Audius platform that caused a total loss of $6M in the community pool of Audius. The hacker posted four governance proposals to the Audius project, and one of them was approved. The fact that hackers are able to steal and sell tokens is a testament to the potential risks of this technology to the interests of the artists and fans involved. In this case, the artist will need to hold and stake tokens to unlock more beneficial features.

What if a more sophisticated hack led to malicious admin proposals to the platform? Users will suffer hefty losses. This is often seen in the cryptocurrency market.

(iv) Let’s be honest here. Fans just want music and that has no problem in Web2

The majority of current users of Music NFT products are crypto-native.

In users’ views, NFT products have high prices, accompanied by other costs such as gas-fee.

Streaming platforms like Spotify are doing just fine by optimizing the experience for both artists and users.

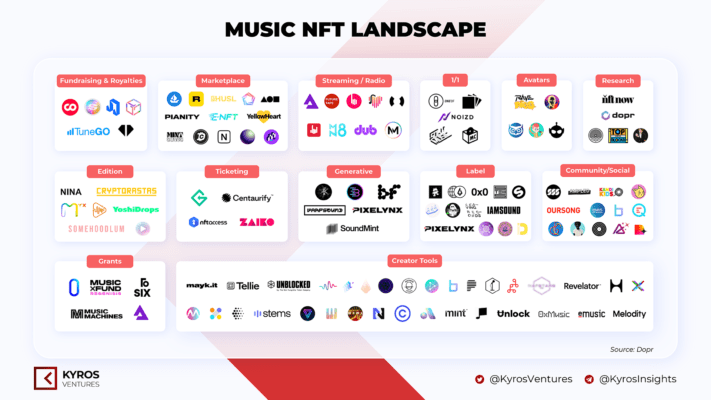

The Music NFT landscape

💡 Web3 is gradually replacing most of the roles in Web2 Music, including both production (Support tools, news and research) and distribution (streaming platform, community, and other logistical tasks required by artist).

Closing thoughts

(i) Small market, good growth, positive experiment with a similar model for Web3 gaming

Music NFT has a total market share of $1.2B, approximately 1/24 times that of the digital music industry which has a total market capitalization of up to $29.4B. On Spotify, there are 11 million artists, and Apple Music with more than 5 million people. So far, the number of artists participating in Web3/NFT in general is just under 30,000 people.

As more and more artists realize that they similarly can become businessmen for the products they create, a form of direct artist-to-fan experience is emerging more than ever. According to the ConsenSys report, the number of Metamask wallet addresses has recently bloomed, reaching 30 million monthly active users, a growth of 600% in just 14 months.

Music NFT paradigm shift is similar to the current GameFi model. More and more people understand and use web3 after the success of GameFi and NFT. Thus, many traditional markets will transform into similar models applied by GameFi. If Music NFT can solve the above concerns effectively, it will be another attractive market for not only artists but also businesses, and fans.

(ii) Web3 sounds great, but we are here for the music. How/when will Web3 music mass adoption?

We learned from GameFi that the game experience should come first, not the monetization factor. Music NFT is no different. The monetization factor plays an incentive role, and we stay for the music.

Behind Spotify and Apple Music’s success stories is the massive data collection and personalization for a better user experience in listening to music and choosing songs.

To do this, Web3 must onboard as many indie artists as possible to join.

Web3 platforms need to provide utmost support for artists’ needs as it’s not only about better income but also more convenience for artists in logistics and product promotion. Let’s assume artists’ work is just performance.

Web3 streaming platforms must be widely promoted, and the apps’ infrastructure must be simple to optimize the user experience.

The more Web3 tooling supports artists, the more artists join Web3. Thus, Web3 will be further enhanced in terms of user data, optimizing like what Web2 is doing now. Then it will be the time for mass adoption.

What is your most painful experience when starting your crypto journey?

Being rugged and scammed? Messing up when trying to distinguish between a passphrase and a private key?

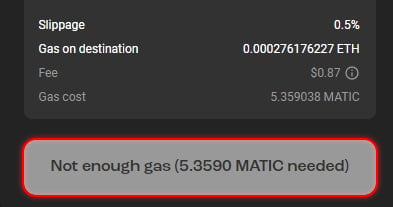

How about the pain of staying up until 3 AM to ape in a potential alpha but then witnessing your transaction fail because of “Not enough gas”?

These are just some of thousands of trouble for crypto newbies. And from here, a solution called “relayer” has been born.

Definition

In blockchain, relayer can be:

(i) A place where individual orders are aggregated to an orderbook for users to store and find matched orders off-chain; only final transaction is submitted on-chain. An example of this is 0x.

(ii) A third party executing transactions on behalf of users and paying platform-native token in exchange for a small fee of service (denominated in other currency).

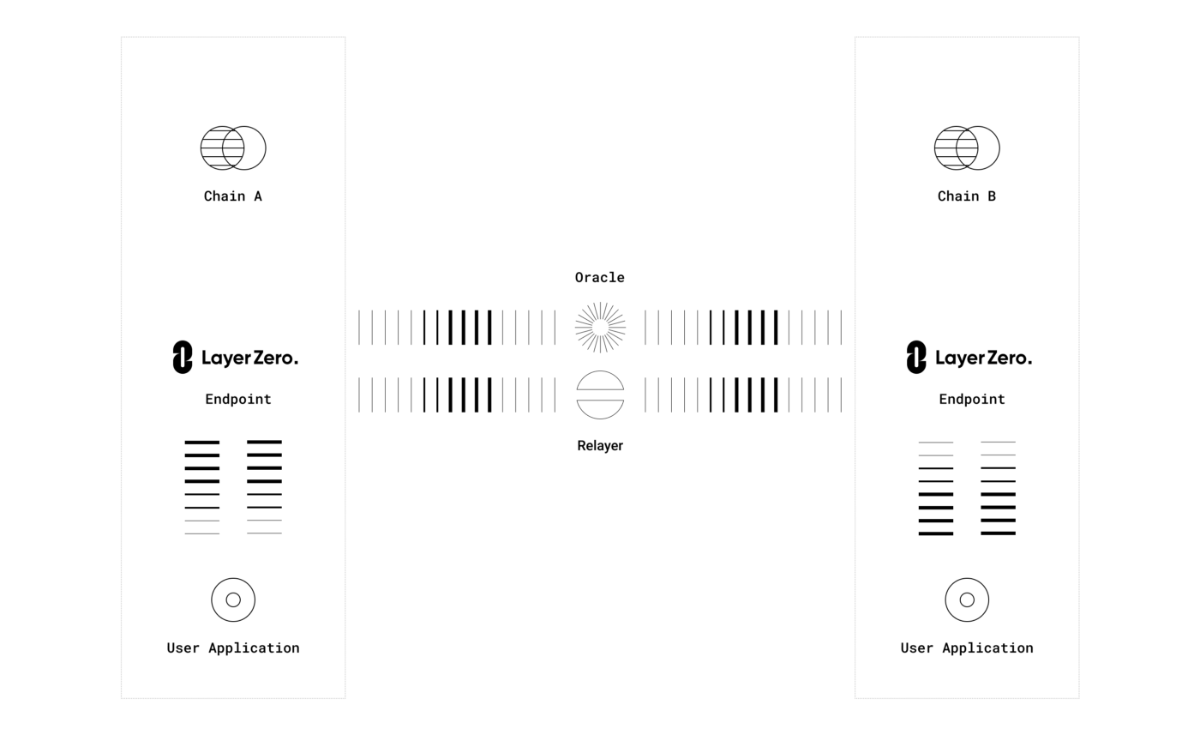

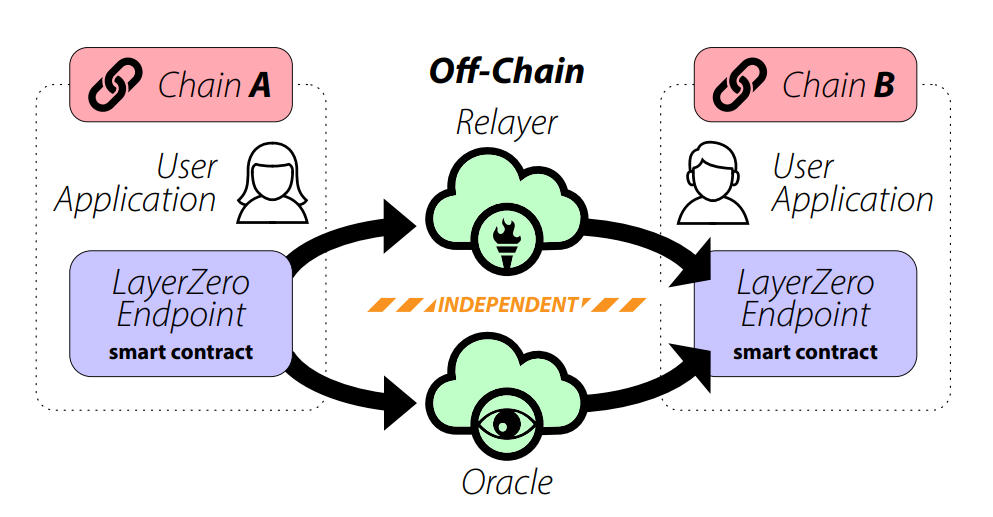

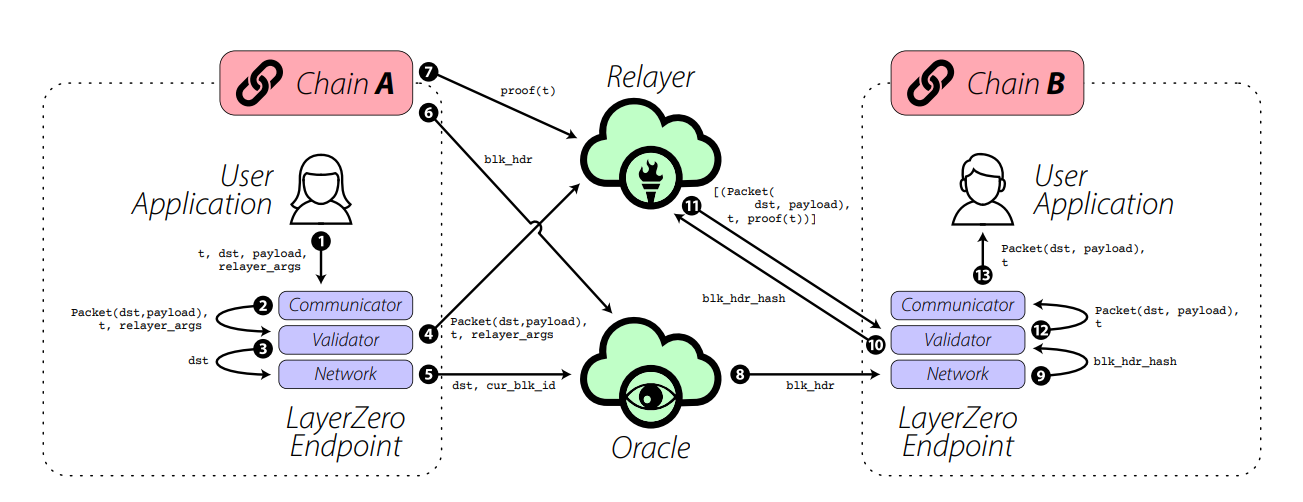

(iii) A third party being in charge of “connecting” different blockchain platforms. These relayers are used in cross-chain projects such as LayerZero or RelayChain.

In this article, we will only discuss the second meaning of a relayer.

Under the hood, such relayer is working based on the so-called meta-transaction, or gasless transaction.

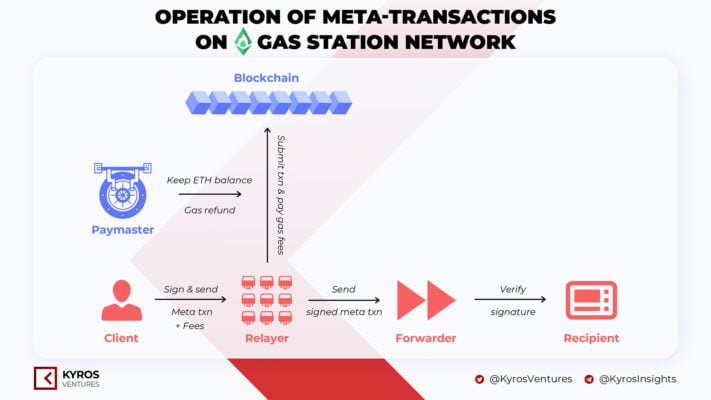

Below is how Gas Station Network (GSN), a system of meta-transaction relayers on Ethereum, operate.

Basically, meta-transactions are transactions in which there is data about an actual transaction inside to be executed which will be created and signed by an individual, and then sent to the relayer. There will be a smart contract (paymaster) responsible for gas payment in exchange for a service fee. A smart contract called forwarder verifies the sender’s signature and forwards the request to a recipient contract. Recipient contract here is the final “destination” where the sender wants to interact with his DApps.

To avoid being criticized the decentralization philosophy of blockchain, relayers and paymasters will work independently and competitively on the network of RelayHub.

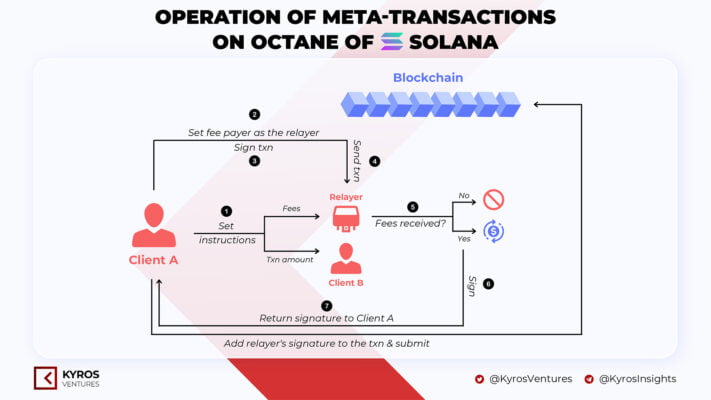

On Solana, the way meta-transactions work is quite different as users can directly specify who the gas payers are. This assignee will have to sign the transaction for it to be approved, thereby reducing the verification and confirmation process of the forwarder as in the GSN system.

Take an example from Octane (in alpha stage), the process occurs as follows:

(i) First, user A will add to their transaction (txn) two instructions: one is to transfer the fee to the relayer, the other is to specify the amount to be transferred to user B (in this case, we need to assume that user A’s wallet has enough funds to pay relayer fees and transfer money to user B, but since there is no SOL available in the wallet, user A needs to go through relayer to send money to user B)

(ii) User A also needs to set the payer as the relayer, instead of him/herself

(iii) User A signs txn

(iv) User A sends this txn to relayer’s API server

(v) Relayer will confirm if it received the fee

(vi) If yes, relayer will sign and send the transaction back to user A

(vii) User A will add the relayer’s signature into the transaction and submit it to the Solana network

Pros and cons of meta-transactions

The main benefit of meta-transactions is the minimalization of user experience when beginning their crypto journey. Users do not need to own any tokens prior to interacting with dApp and web3. The use of meta-transactions may not require non-custodial wallet but developers would need a key storage system or password that removes technical obstacles of such decentralized wallet. Moreover, having a third-party for transaction settlement can help reduce some burdens on the blockchain network as mutiple transactions from a DApp can be processed off-chain and finalized to only one transaction to submit on-chain.

However, meta-transaction relayers still face two big drawbacks:

Not all smart contracts support meta-transactions

Although these protocols can use a network of relayers to decentralize the process of validating transactions, this cannot totally guarantee that the network will be secure and that there will be no corruption among relayer servers

Why relayer is important in crypto?

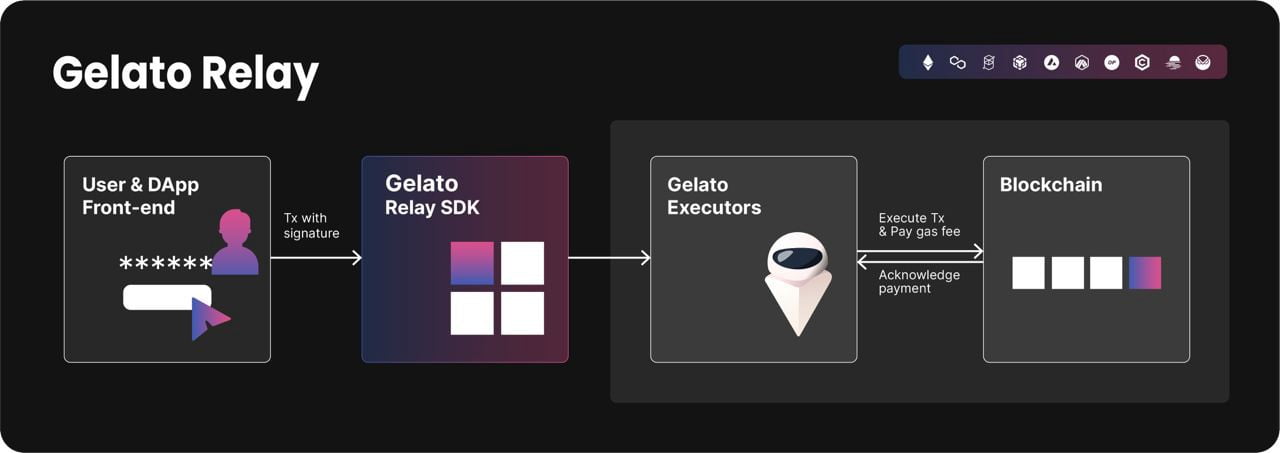

Besides GSN, some other DeFi protocols do apply meta-transactions to make their UX smoother. Zero Swap, a liquidity aggregator from AMMs on 0x, or Colony, an infrastructure project for DAOs have utilized meta-transactions. Gelato Network, a decentralized network of bots for automatic execution of smart contracts, has implemented meta-transaction in their infrastructure. Gelato connects developers who need to automate their smart contracts with the infrastructure operators who are responsible for running bots to receive corresponding service fees. To complete user request, Gelato needs to pay gas fee to interact with the blockchain, and meta-transaction relayer will be used here to fulfill such tasks.

However, building an in-house system of meta-transaction relayers for meta-transaction will consume a lot of resources in terms of time and effort for crypto projects. Therefore, there are meta-transactions solutions built to optimize this process, of which the most prominent names are GSN (mentioned above) and Biconomy.

Biconomy supports both DeFi and NFT meta-transactions. One of their three main products – Gasless Transactions – allow projects to sponsor their users for gas fees – either it is DeFi or NFT transaction. In August 2021, the fashion brand D&G and UNXD, an NFT platform for luxury products have collaborated with Biconomy to launch the Glass Box NFT project, including NFTs which give users access to their metaverse as well as real-life benefits from D&G.

In the beginning of this year, 100Thieves, a lifestyle brand, has also worked with Biconomy for a free NFT airdrop to their community.

Conclusion

Although relayers still have a few disadvantages that need to be overcome, its role in making the experience on DApps less “bumpy” is undeniably important, especially in the context of crypto projects that are having a hard time expanding their customer base due to high technical knowledge required by these users.

Building a relayer can be compared to building an automatic toll collection. Although it is expensive and labor-intensive at first, the benefits of traffic infrastructure and network connection will be smoother and more efficient in the future.

This article serves the purpose of expressing our arguments on a data-based view of the fundraising market over time to present an outlook for the potential growth of different categories within the cryptocurrency market in the upcoming years.

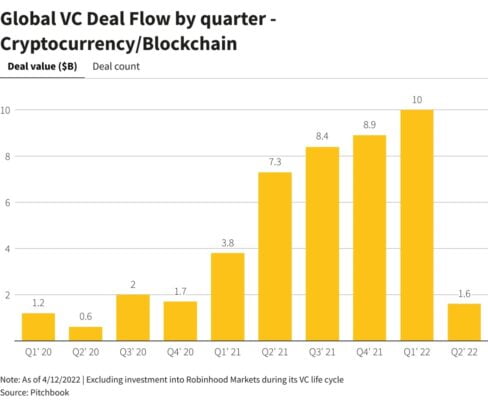

The last quarter of 2022 has set a new record for the amount of capital raised in the crypto industry, recorded at $10B, thereby showing a great expectation of venture capital funds for this dynamic market.

The fact that billions of dollars are poured into blockchain startups is still leaving many doubts among investors as to whether this is a “crypto bubble” and whether cryptocurrency assets are being traded at an unreasonable and unsustainable price?

We’ll compare the fundraising market in bull/bear market cycles to answer this question. Here, we will distinguish funding rounds according to 2 main stages: Pre-mature and Mature.

Stage

Including

Pre-mature

Pre-seed round

Seed round

Strategic round

Mature round

Series round

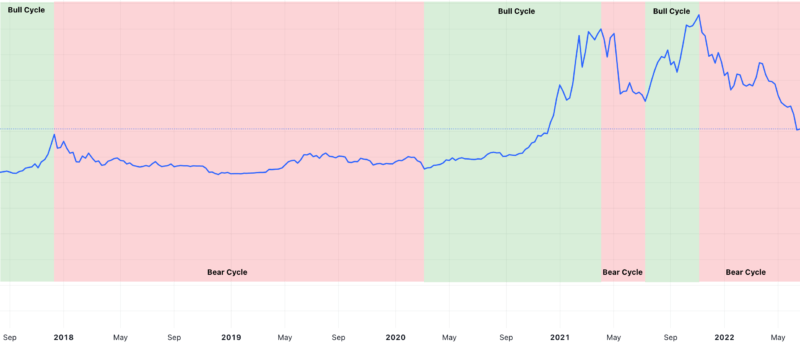

Market Cycle

Market cycles refers to a trend or pattern that occurs during different market periods or trading environments. Market cycles are made up of two aspects, the highest and the lowest price, and the current cryptocurrency market is affected by Bitcoin price.

In each market cycle, we often see trends forming in a particular sector/category due to outgrowth innovation, leading to some asset classes becoming dominant because their business conditions are suitable for growing conditions.

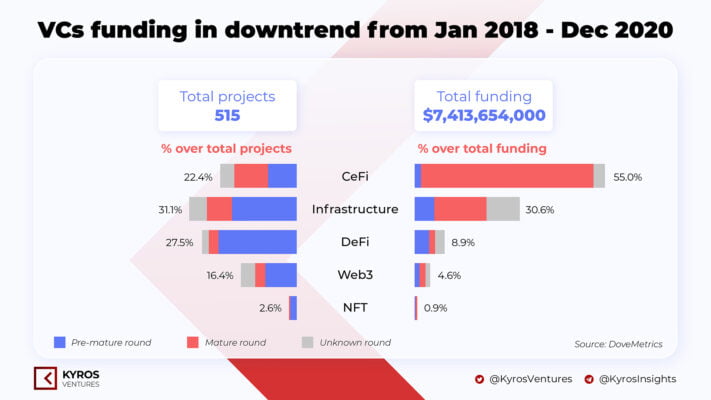

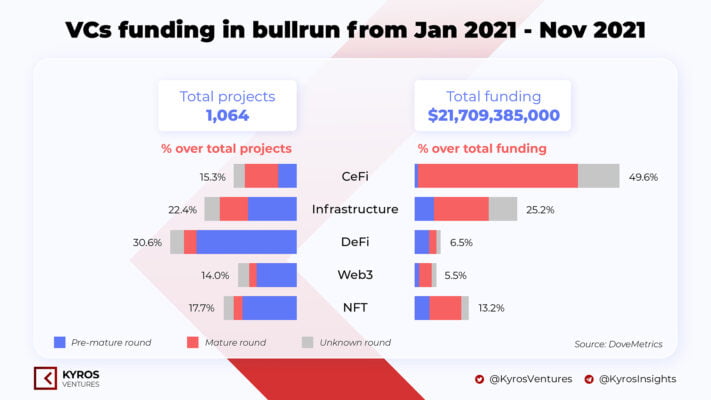

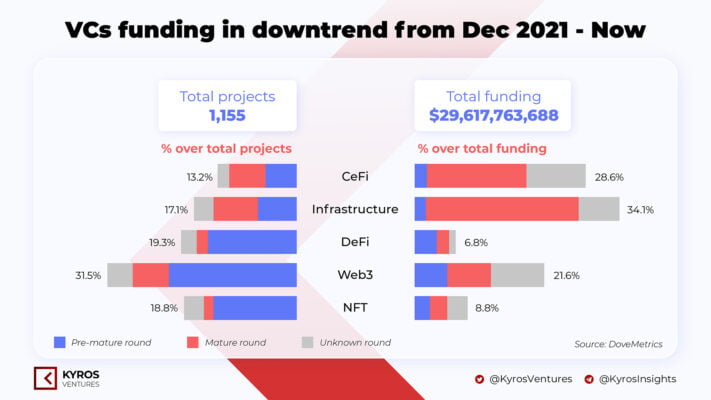

Here we will discuss five main groups of capital market categories, including Infrastructure, CeFi, DeFi, Web3, NFT, according to data obtained from Dove Metrics.

Capital Flow

Building the Infrastructure

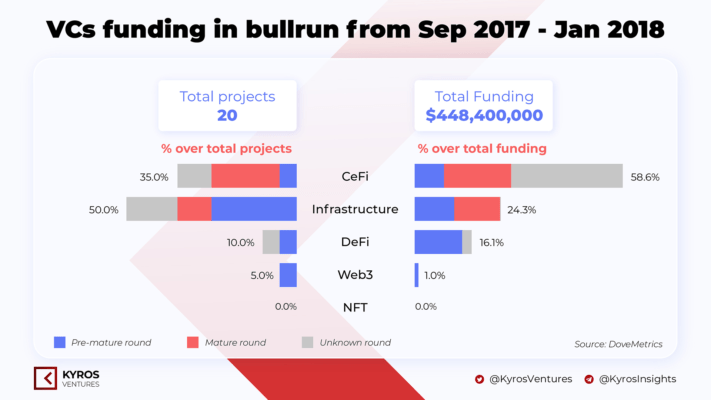

2017 was the stage of blockchain application incubation and CeFi then was the safe choice for venture capital funds when it received the most investment and five out of eight projects came from the expansion and growth phase (series rounds). Since CeFi projects have an operation model more similar to those of traditional businesses, VCs can partially rest assured that their investment in these series rounds can potentially make some returns.

New decentralized applications (dApps) began to form during this period since the opening of the first smart contract platform, Ethereum. Thus, this is the period when VCs prioritise spraying capital for infrastructure projects as the foundational platforms are still in their infancy; moreover, this will be the first and best place to attract liquidity when dApps are built on top of them and bring viable adoption to blockchain technology.

As many smart contract platforms were built to solve the current scalability problem of Ethereum, notably Cardano, Solana, Polkadot, etc., the next destination will be the building of the economy for users. Although CeFi is still the category that received the most investments during 2018 – 2020, Infrastructure and DeFi are the two categories with the most projects receiving investment, especially projects from pre-mature rounds.

Since mid-2019, DeFi has been raised as an alternative solution for traditional banks, allowing users to transact, save and earn profits based on banking-like but non-banking financial services. Many of DeFi solutions are novel and can offer higher returns than the centralized financial market.

The DeFi wave rose shortly after June 2020 which was catalyzed by the launch of the liquidity farming program $COMP, the governance token of Compound in May 2020. The event also kicks off the DeFi Summer, when other DeFi projects distribute their tokens through liquidity mining and create more and more profit opportunities for their investors.

Afterwards, the number of DeFi projects have been continuously rising, therefore capturing attention from VCs. By the end of 2020, DeFi took the lead in the number of projects being invested. At this time, VCs showed great confidence in this new category and thus, raising the bet for this category in hope of enormous returns.

Building ownership application

With DeFi providing a decentralized exchange solution for users, NFT emerged as a solution for content creators in areas such as music, pictures, or other artistic content. NFT is a unique asset class applied to digital assets as an intellectual property license.

By 2021, NFT was getting a lot of attention from investment funds as NFT collections like CryptoPunks, Bored Ape Yacht Club have attracted mainstream media and these projects reach the level of billion-dollar valuation.

As of May 2021, only 72 projects in the NFTs segment have successfully secured their fundraising with a total funding value of $777M compared to 180 DeFi projects at a total value of $645M. However, this number has changed significantly by the end of the year since the amount of money raised for NFT-related projects only in pre-mature rounds has risen to the 2nd place – with 151 more projects being funded.

What can we see from past data?

Capital flows from venture capital funds exemplify the appropriate development of the market, beginning with the formation of the underlying platform (Infrastructure), followed by the creation of an economic system (DeFi), and then applications for content ownership (NFT).

Infrastructure → Economic system (DeFi) → Content Ownership (NFT)

In each stage of the market, new categories are created and will be the trend to lead the market in terms of capital flow as well as the number of new projects being born. Categories that are incubated and developed after each market cycle tend to grow more stably, and as a result, their ROI for VCs will be more saturated.

What’s coming next?

The success of the Infrastructure category has caused a gradual shift of many VCs from the segment of CeFi to Infrastructure, reflected in the total amount of capital that this category has raised in expansion rounds. The number of Infrastructure projects going into operation and revenue expansion increases, opening up a more stable, long-term profits for VCs when pouring capital into such viable models.

Besides, the smart contract platform system has entered the stage of stable development and is able to scale to a large number of users; the next possibility will be in layer applications. Prominent in the second half of 2022 came from Web3 applications, more specifically GameFi like Axie Infinity which created a massive wave of attracting many users to enter the market.

This has driven the Web3 category to receive more attention from VCs in the past two quarters, accounting for 31.5% of the total invested projects. This has driven the Web3 category to receive more attention from VCs in the past two quarters, accounting for 31.5% of the total invested projects. Web3 is currently leading in the number of projects, and the amount of money raised for pre-mature rounds. Primarily, GameFi/Metaverse accounted for 49.8% of the total number of projects funded in the Web3 category (source: DoveMetrics).

With more and more people using NFTs, these digital assets are heralding a new era of the digital world – the Metaverse era. GameFi/Metaverse can be a gateway with a more accessible approach for the masses who are not into or understand blockchain products. Web3 application layer is a combination of DeFi and NFT, an upgrade of User-Generated Content platforms like Facebook, Youtube, etc. Users can now own the content they created on Web3 and can be traded based on their demands without being controlled by any other third parties.

Besides, Web3 promises to bring many benefits for enterprises, including reducing operation processes and lowering expenses when accessing user data. Traditional gaming studios have proven this when moving their businesses up on Web3.

In conclustion, the metaverse is formed by a collection of countless user data, and every user would only want to protect their privacy, i.e. not allowing it to be centralized or owned by third-party businesses or individuals. Therefore, web3 is considered as an open gate for the realization of the metaverse through a decentralized system.

During this bearish phase of the market, as the father of Web2 – Tim O’Reilly believes that Web3 would really emerge after the burst of the crypto bubble, with the backing from VCs, quality projects in the web3 niche, especially the infrastructure platforms serving the metaverse like GameFi and will have great potential to skyrocket in the future. In addition, many other Web3 projects are working on the music industry and social networks, etc., all have similar potential that we should look forward to.

Examples used in this blog are simplified to help make technical concepts more understandable to our audiences. Therefore, please embrace them with an open mind.

Five o’clock in the morning.

Annoyingly loud police siren in front of the house.

“You’re arrested”.

Jack woke up and could not understand what was happening. Everything was like a real-life nightmare.

He was drawn out and treated as a criminal.

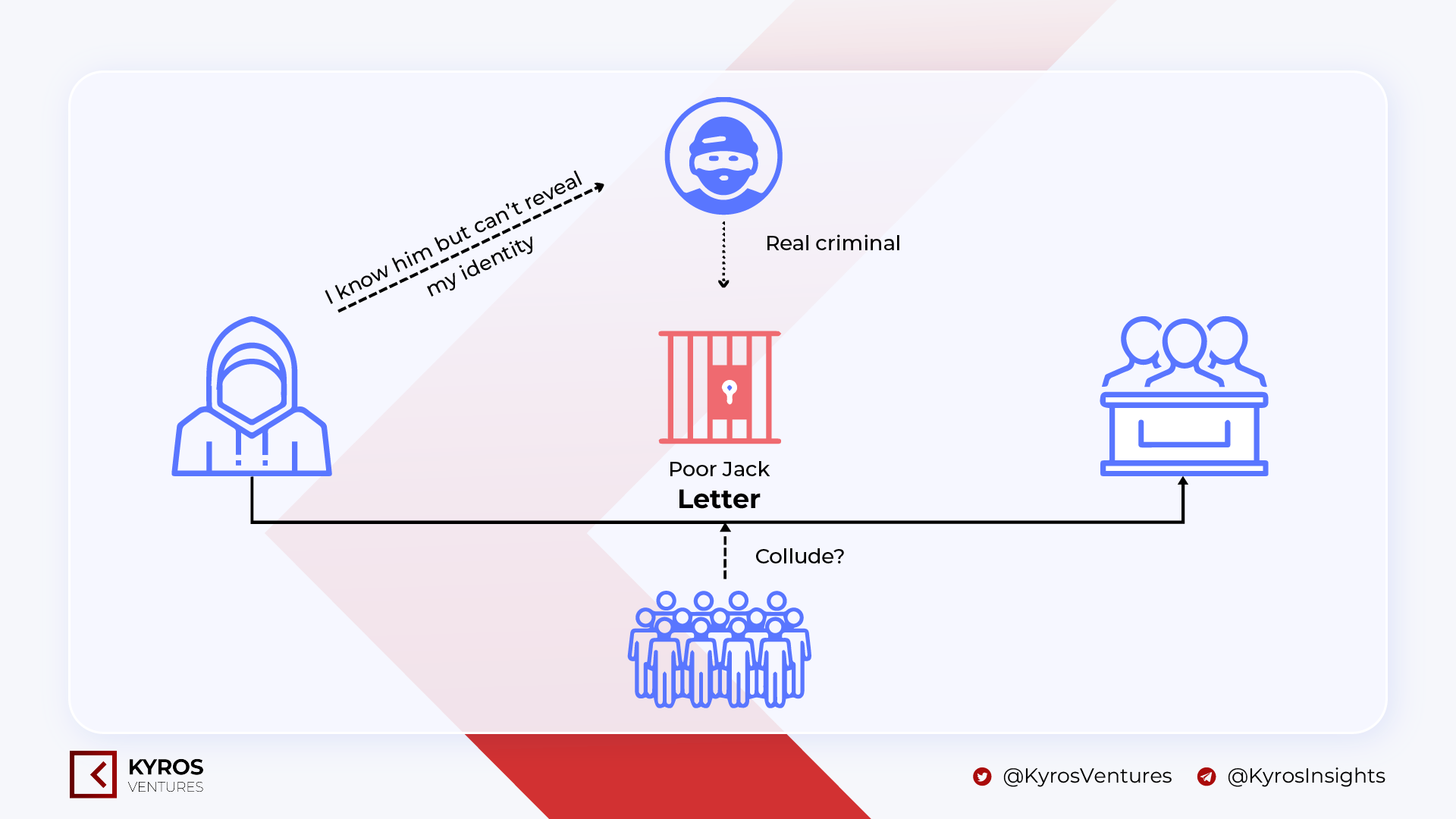

Totally helpless. He was innocent, but then how come his age, his date of birth, and even his bank account number all coincided with those of the criminal, just like somebody else has lived his life.

A stolen life.

The privacy of Jack has been severely violated, and now he is facing imprisonment for the rest of his life. Nevertheless, surprisingly, just days before the verdict is brought in, the jury has received an anonymous letter saying that Jack was not the true criminal and that the writer knows where the true criminal is but cannot reveal the name directly in this letter. If the jury and the letter’s writer arrange a private meeting, it will be difficult to make sure that they do not collude to accuse another innocent person of committing this crime.

Then how can the anonymous writer secretly reveal the true identity of the criminal to the jury in a more transparent manner?

Transparency can be ensured by blockchain, and privacy can be satisfied through some more specific mechanisms.

In this blog, we will introduce our readers to the mechanisms currently being used by some blockchain platforms to ensure the privacy of users in their networks.

Trusted Execution Environments (TEEs)

Basically, in a Trusted Execution Environment (TEE), the data will be isolated from other parts of the processor, thereby protecting them from attacks from outside actors. Regarding blockchain, this means that validators cannot reach the data computation under the hood when they are being used. Secret Network and Oasis Network are the platform blockchains that use this technology, specifically the SGX (Software Guard Extensions) processor of Intel, dedicated to providing a TEE for sensitive data.

Therefore, if the anonymous writer contacted the jury to reveal information about the real culprit through such blockchain platforms, he would not need to worry much about either the authenticity of the content in the letter to the jury or the information leakage as it is protected within the TEEs and the public can rest assured that neither party – the writer or the jury – are colluding to blame anyone else for doing the crimes.

However, there are still issues with TEEs. The SGX processor assumes that only the central processing unit (CPU) is trusted, so storing confidential information here and isolating them would be a safe solution. Taking advantage of this assumption, hackers will not directly attack the computer’s security system but instead take a bypass, attacking other channels of the system. This process can also be known as a side-channel attack.1

Another problem when applying TEEs in the blockchain is rollback attack. The main cause of this problem is that the state of a blockchain can always be rewinded, and the “privacy” provided by TEEs only exacerbates the issue,2 allowing them to leak confidential data to other people.

Mix-up

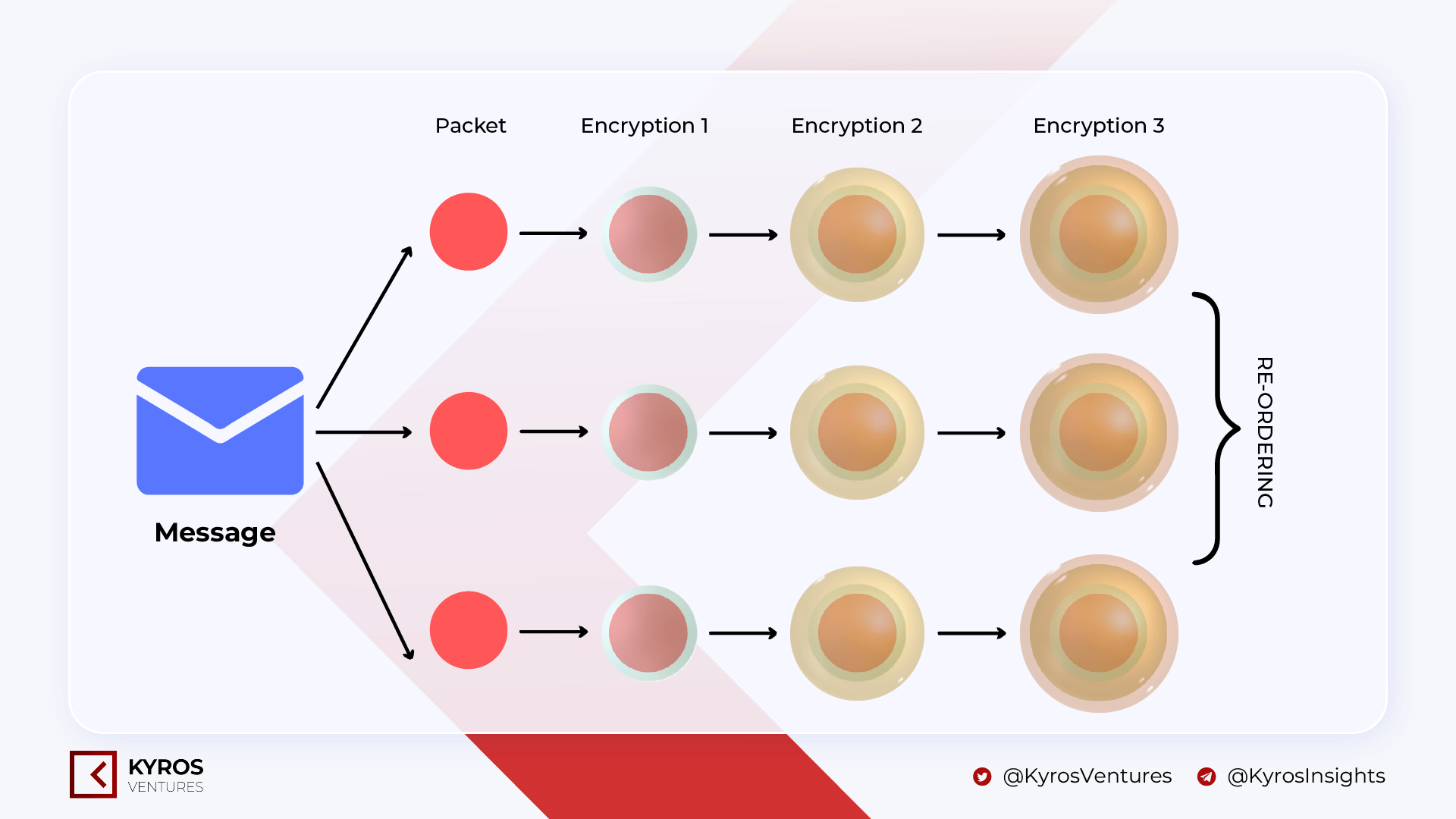

Mixnet is a mechanism used by the NYM Network. In the mixnet, the route of transactions will be “erased”, making it impossible for outsiders to find out detailed information of these transactions.

The mixnet is like an upgraded version of Onion Routing, a method of ensuring anonymity when communicating within a computer system. In this method, a message will be divided into many small packets, and these small packets will be encrypted through many layers in the process of being delivered to the destination. Mixnet goes a step further with this approach by re-ordering the encrypted packets, making it even harder to decrypt the original message.

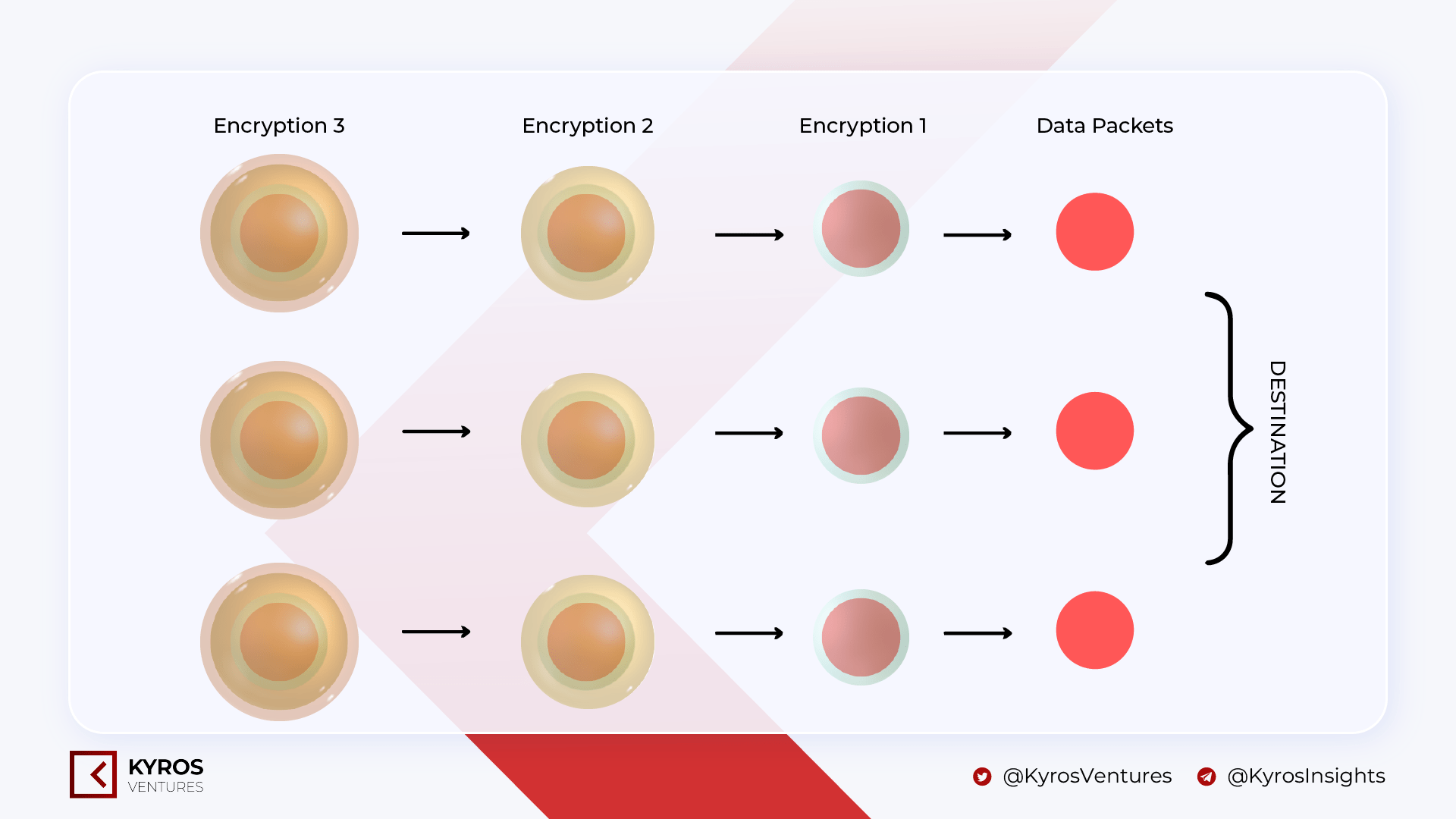

After arriving at the destination, layers of encryption will be peeled off and arranged to the original for the sake of decrypting the original message.

For the anonymous writer, he would write a letter revealing the identity of the true criminal to the jury, then tear them down, mix them up and pack those pieces with three layers of envelopes and three special glues. Each time they pass through a mail station, only one layer of envelope will be peeled off. When all of these pieces reach the jury’s mailbox, the last envelope will be completely removed, and there will be a small hint for the jury to rearrange them in their right order so that they can read the original message.

Another transparency mechanism of this type is also used by Tornado Cash. Tornado Cash improves transaction privacy by breaking the on-chain link between the source and destination addresses. It uses a smart contract that accepts deposits of ETH and other tokens from one address and allows them to withdraw funds from another. When the transaction is completed, the transaction route from the sender to the receiver will be broken. However, privacy in this mechanism cannot be guaranteed absolutely.3

Ring Signatures

This is a method used by Monero, one of the pioneering privacy blockchain platforms in the space.

Back to Jack’s story, there will be an additional detail which says that the anonymous sender is actually a member of the Triads, whose leader is the real culprit in the crime which Jack is facing. The anonymous sender is feeling guilty and he wants to tell the truth but does not want to reveal his identity. On behalf of the Triads gang, he collected the public keys of its members and combined them with his private key to sign the letter sent to the jury. Thus, the jury can be confident that this letter was written by a member of the Triad, but no one, including other members of the gang, could know the identity of the sender of this letter.

The example above is a simplified demonstration of how ring signatures operate.

In the Monero network, privacy is also ensured through the use of stealth addresses. Stealth addresses are used both by the sender and recipient and can be used for only one time.

Zero-knowledge proof (ZKP)

This is a unique technology that helps an individual prove that he or she knows a certain truth without having to say it directly.

A fairly popular development branch of ZKP today is ZK-SNARKs. Examples of projects using zk-SNARKs include ZCash and Mina.

zk-SNARK refers to a structure in which a prover can prove the possession of some information via a secret key without disclosing that information and without any interaction between the prover and the verifier.

With the “non-interactive” structure, the cryptographic proof is only transferred once from the prover to the verifier but many times compared to the traditional method of ZKP.

In the case of the anonymous writer, when sending another letter to the jury to reveal the real identity of the criminal, he would only need to attach a cryptographic on the blockchain to prove to the public that what he knows about the criminal is completely true, and that he did not secretly communicate with the jury to blame other innocent people.

Currently, the most efficient way to create a zero-knowledge proof that has a “non-interactive” structure and is short enough to be published on the blockchain is for a structure to have an initial setup phase with a chain of references being shared between the system and the validators, known as the system’s public reference number.

Until recently, another variant of SNARKs emerged to mitigate the existing drawbacks in this technology: zk-STARKs. This solution has been developed by StarkWare, one of the famous layer 2 solutions for Ethereum.

STARK allows developers to move the computation and storage off-chain. These proofs are then put back on the chain so that any interested party can validate the calculation. Moving the bulk of the computation off-chain using STARKs allows the existing blockchain infrastructure to scale more quickly and efficiently. However, the size of the cryptographic proof of the zk-STARKs is larger than that of the zk-SNARKs, which on the one hand makes it less vulnerable to quantum computer algorithms but at the same time make it heavier for the memory space than zk-SNARKs.

A cataclysm called the “Global Financial crisis” swept through the globe, leaving a massive shock for the entire financial markets, especially the banking and real estate industry. The crisis then eroded people’s trust in a centralized and bureaucratic financial system with plenty of vulnerabilities.

From this erosion of trust, there came the invention of the blockchain, marking the beginning of a new era in the technological revolution.

In this world, each blockchain platform is seen as an independent country where the gas fees are their living costs and their consensus mechanism is regarded as a type of political philosophy.

This blog post does not intend to wireframe your point of view into any specific countries or political organizations in the real world. We hope the audience can take an open view with these disclaimers in mind and enjoy the comparisons provided here. Thank you.

The Paleozoic Era: Bitcoin

Blockchain was first termed in 1991 by the two scientists Stuart Haber and Scott Stornetta in the article “How to timestamp a document digitally”.

It was until 2008 that blockchain was popularized when one of its first major applications, Bitcoin, a peer-to-peer electronic cash system, was introduced to the world by a person named Satoshi Nakamoto. The purpose of Bitcoin is to solve the double-spending problem without the need for a trusted authority or any centralized entities.

Bitcoin has always dominated in terms of the very first cryptocurrency built on blockchain thanks to its decentralised consensus. The recent expansion of Bitcoin and blockchain has led legislators and investors in the traditional financial world to see them as a threat to the country’s staunch anti-money laundering system. But at the same time, they also consider this a potential ground for new investment opportunities and break out of the old-fashioned investment channels whose profits are already saturated.

While Bitcoin is the most powerful country in the blockchain world, it is still not an ideal location for creating economic activities for society. One of Bitcoin’s most important legacies is its political philosophy – Proof-of-Work. Other countries, such as RSK, DefiChain or Stacks, have contributed to bringing new vitality to Bitcoin by allowing its users to participate in activities in their own country while still securing them through a direct connection to Bitcoin.

EVM Union: Where Civilization Begins

Although Bitcoin has a big influence on the blockchain world, Ethereum takes the lead in terms of prosperity. Ethereum, founded by Vitalik Buterin in 2013, created a new political philosophy called Proof-of-Stake with its administrative apparatus, called the Ethereum Virtual Machine (EVM). Many countries that came out later used this administrative apparatus, thereby forming the EVM Union.

The purpose of EVM is to serve as a runtime environment for smart contracts built on Ethereum which is a new way to build decentralized applications.

Another reality that plays out on Ethereum is that although the country leads in prosperity, it also leads in terms of the living costs. The fees that users need to pay when building and living on Ethereum range from $5 to $100 depending on different activities (not to mention peak hours), much higher than in other countries. The high standard of living comes from so many activities happening there where resources and land only exist as a limited amount.

As a result, the products on Ethereum (i.e., the blockspace) experienced a severe imbalance between supply and demand. To solve this problem, many other blockchains have been built around Ethereum to reduce the crowded activities on the land. These countries are categorized based on the infrastructure they use to offload activities on Ethereum, including each of the following subgroups:

Optimistic Rollup: This is where transactions are bundled together (to save space and costs) and are validated by default. The system will have a reward mechanism for those who can prove that these frauds are genuine. Nations of this group are Arbitrum, Optimism, Boba Network, and Metis.

ZK Rollup: This scalability solution works almost similarly to Optimistic Rollup, but cryptographic proofs are used to prevent frauds more proactively. Starkware, zkSync, and Immutable X belong to this group.

State channels: First transaction is settled on the chain, opening up a new channel so that in-between transactions are settled off-chain and secured by a multi-sig system; then, when the interaction between two parties ends, the last transaction will be settled on the chain. Connext, Perun, Raiden, and State Channels are members of this group.

Sidechain: These countries have their own political philosophy, running in parallel and connected to Ethereum through a bridge. Countries under this category are Polygon, Palm, Ronin, and Gnosis Chain.

Plasma: Countries in this group may have their own political philosophy but derive security from Ethereum through fraud proofs. They are different from sidechain in the sense that everytime they finish sanctioning a resolution, they will submit this sanction to the Ethereum mainnet. OMG Network belongs to this group.

Validium: Validium countries like StarkEx or zkPorter secure transactions that take place in their countries through cryptographic proof with the computation data being stored off-chain.

BNB Chain

Despite being built on forks of Tendermint and Cosmos SDK, BNB Chain belongs to the EVM Union. This explains why the BNB Chain is placed inside the EVM Union and next to the Cosmos continent.

Being backed by the largest crypto exchange in the world, Binance, it is no surprise that this nation stands in the top 2 of TVL with multiple high-quality projects. Besides, it is a country of GameFi projects. This place has all it needs for a GameFi project to take off:

A vibrant community

A secure and liquid NFT marketplace

Cheap cost and fast transaction for users

Huge support from the Binance team itself

BNB Chain follows the Proof-of-Authority and Delegated Proof-of-Stake (Delegated Proof-of-Stake) philosophy to help its operations run smoothly while maintaining a reasonable living cost.

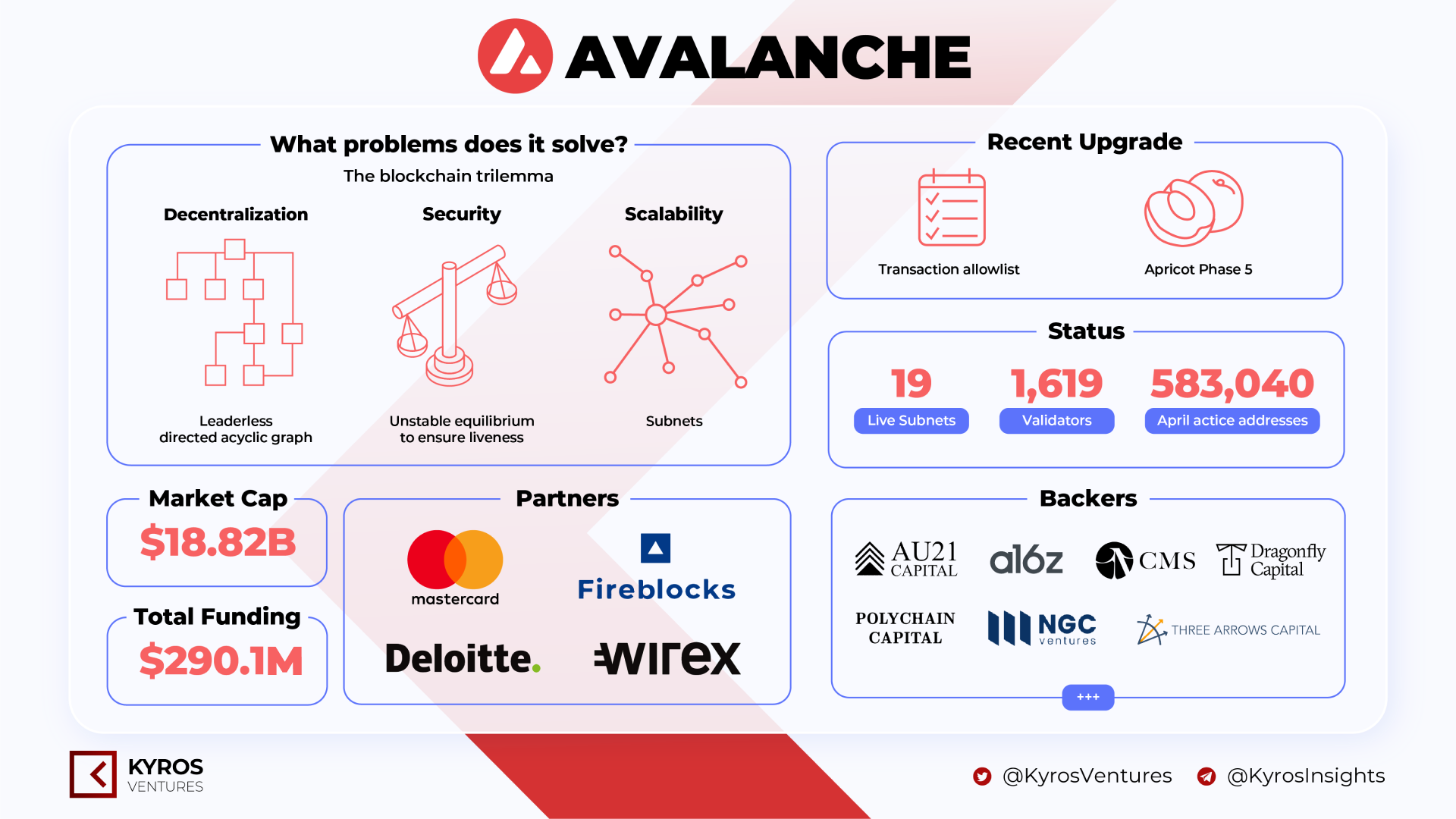

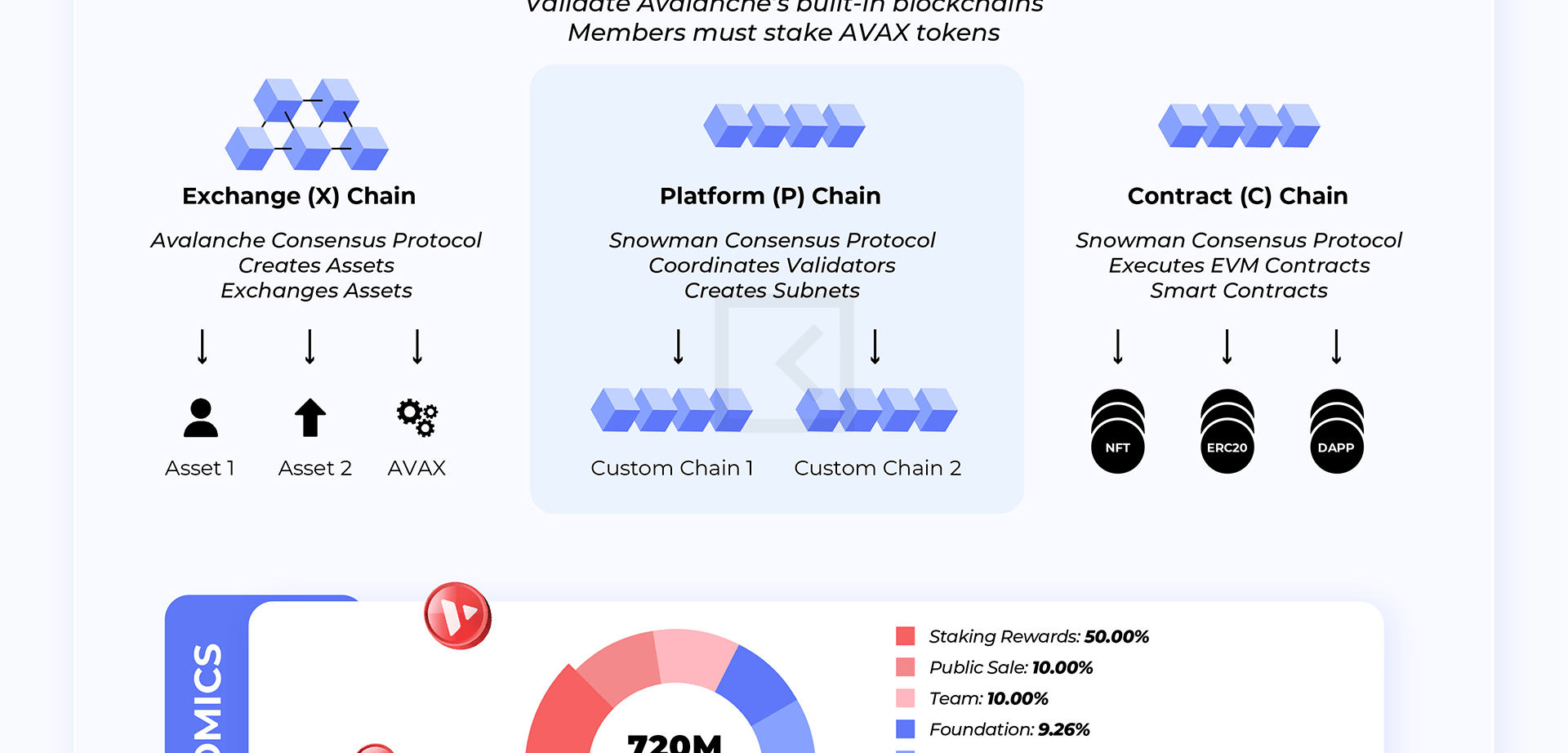

Avalanche

Another Chad in the EVM Union is Avalanche. Only launched in 2020, this country has quickly risen to be the third-largest in the Union. The superb design in its political philosophy plays a vital role in bringing Avalanche to this position when it has attracted plenty of human and financial capital resources. Avalanche also aims to be a sovereign country with multiple subnets being built around it. The first two countries in this sovereignty are Defi Kingdoms, a well-known game title originating from Harmony but still in this EVM Union. The other is Swimmer Network, born from the most played game on Avalanche Crabada.

Avalanche does have its own Executive Branch – Avalanche Virtual Machine. X-Chain, the chain which is in charge of asset creation and exchange, is an instance of AVM.

Fantom

Starting with an idea of modular architecture, Fantom is a country that makes it easy for immigrants to live, integrate and adapt to the lifestyle here. It has attracted a lot of migrants and enriched its land, and is now ranked fourth in the EVM Union.

Nevertheless, Fantom encountered a crisis earlier in 2022 stemming from the demise of Solidex, a project that was running on Fantom at the time, and the departure of Andre Cronje, the person behind the formation of Fantom. Most recently, a lending institution in this nation, Deus Finance, was attacked by hackers, leading to the degradation of life quality and severe brain drain as users migrated to new and safer lands.

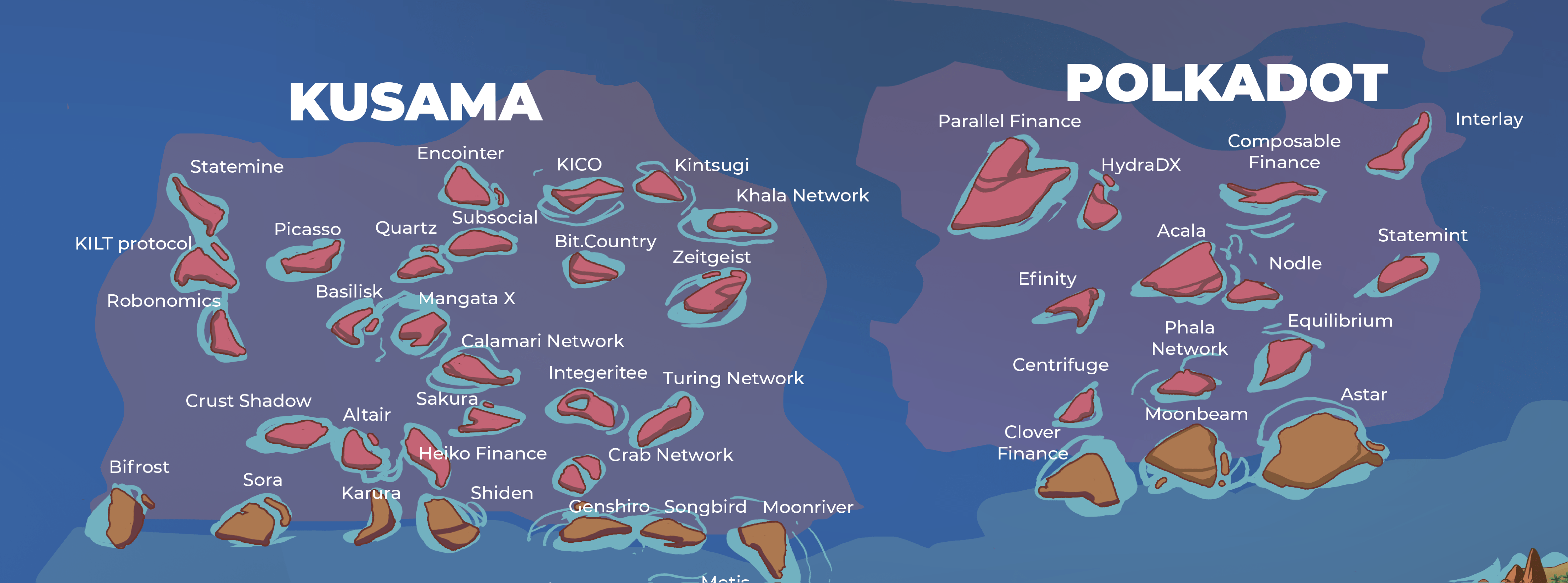

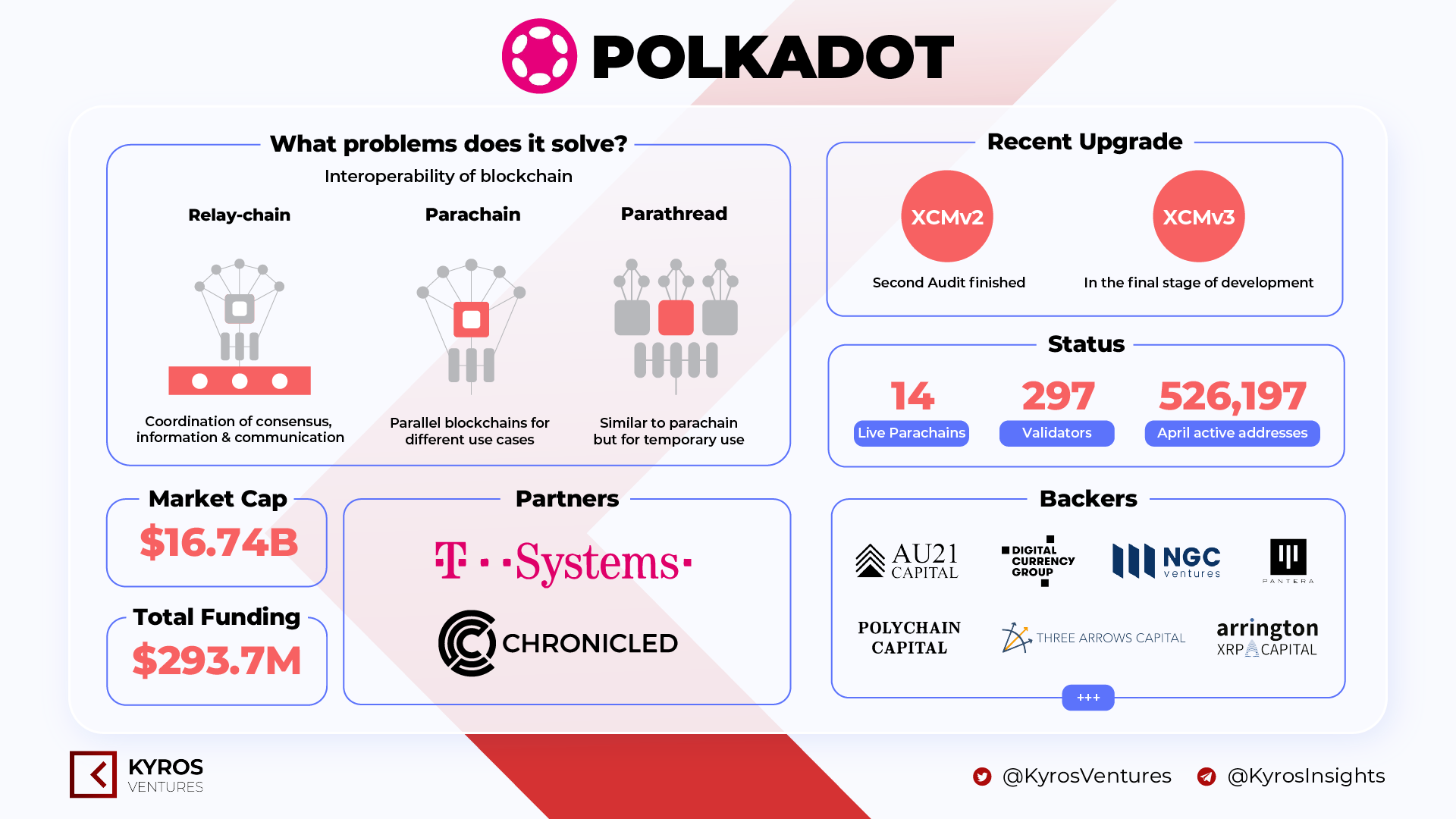

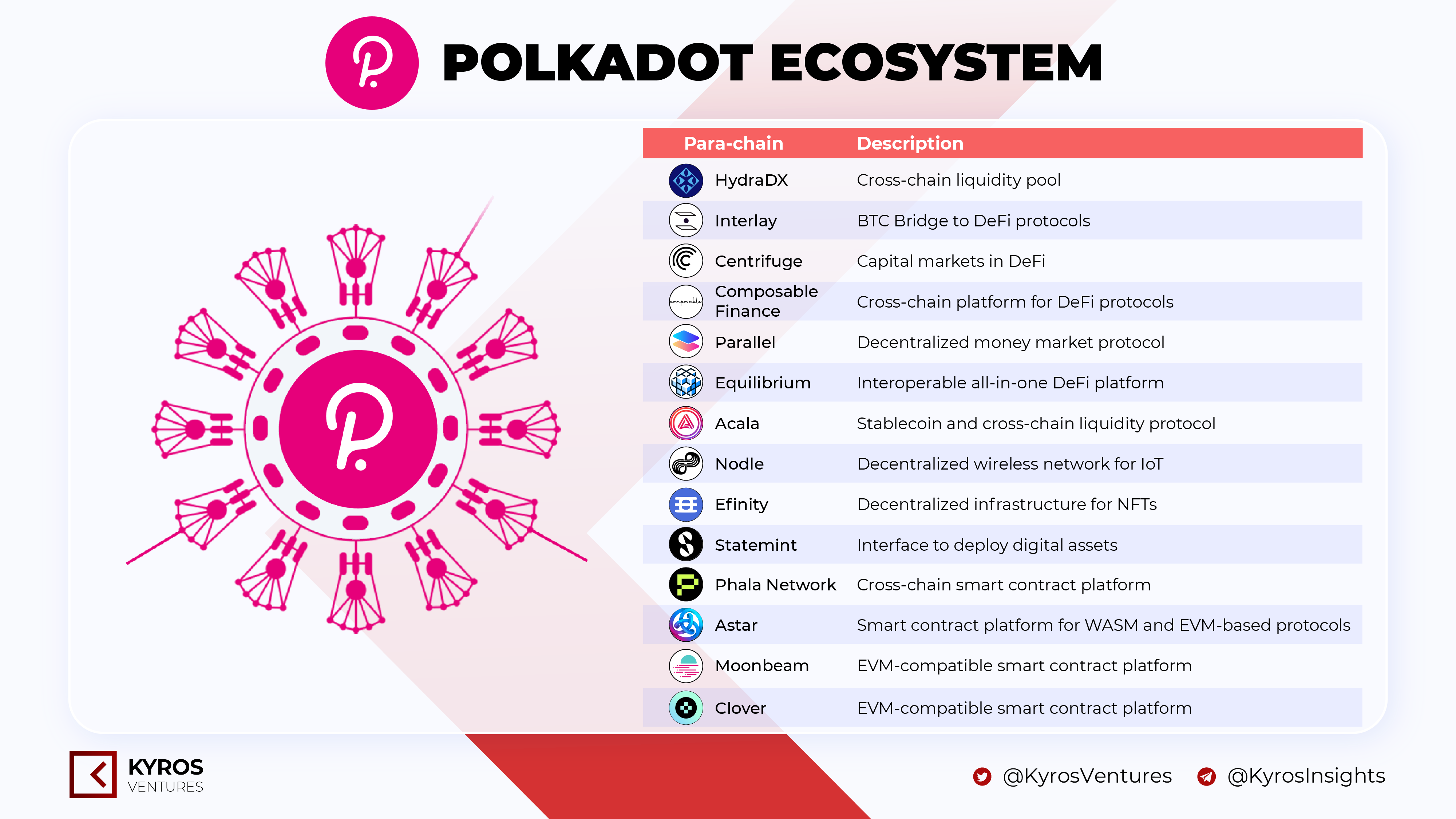

Polkadot: The rise of multi-chain

Ethereum and Vitalik Buterin’s Smart Contracts have revolutionized the blockchain world, but that doesn’t seem to be enough to keep Gavin Wood, once a co-founder of Ethereum, staying and contributing to Ethereum. In 2016, Gavin Wood left for a new adventure to conquer new lands that can pursue the “decentralization” mandate of blockchain.

That is how Polkadot was formed.

Unlike Ethereum, where all vitality and activities take place on a single platform, Polkadot allows the birth of many satellite countries to exist in parallel as an extension country, thereby reducing the workload pressure that Polkadot has to handle. Relay-chain is at the heart of Polkadot. All activities are coordinated through a relay-chain with many para-chains, which are satellite countries, surrounding this centre to exchange and receive security from the force of validators gathered here. Currently, a total of 14 countries exist on this Polkadot continent. Each country pursues a different goal to achieve the final objective of diversifying the continent’s ecosystem: Efinity focuses on infrastructure for NFTs; Astar, Phala Network, Clover or Moonbeam focuses on infrastructure for Smart Contracts; Nodle focuses on blockchain infrastructure for IoT (Internet of Things) technology; Statemint serves the deployment of digital assets on the Polkadot network; while HydraDX, Interlay, Cetrifuge, Composable Finance, Parallel, Equilibrium and Acala focus on DeFi.

Kusama is a strip of a continent connected to Polkadot. Therefore, this continent is built for users to have a creative environment and test their ideas before officially deploying on Polkadot. Although often being seen as a “simulation” environment of Polkadot, Kusama still has its own habitat for people to participate in the construction and a separate economic system that everyone must follow while living here. Currently, 29 countries exist in this territory.

Cosmos: A universe of blockchains coming to reality?

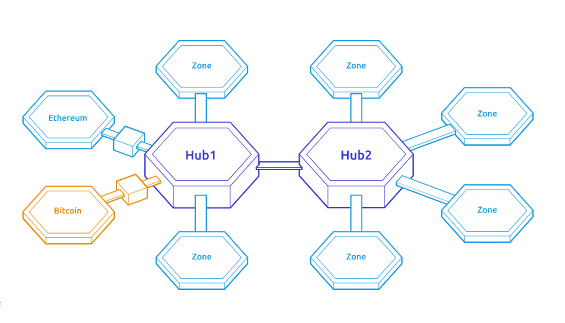

Regarding a scalability solution for Ethereum, Polkadot or Avalanche is not the first country to introduce the concept of multi-blockchain on a territory; Cosmos has previously thought of it.

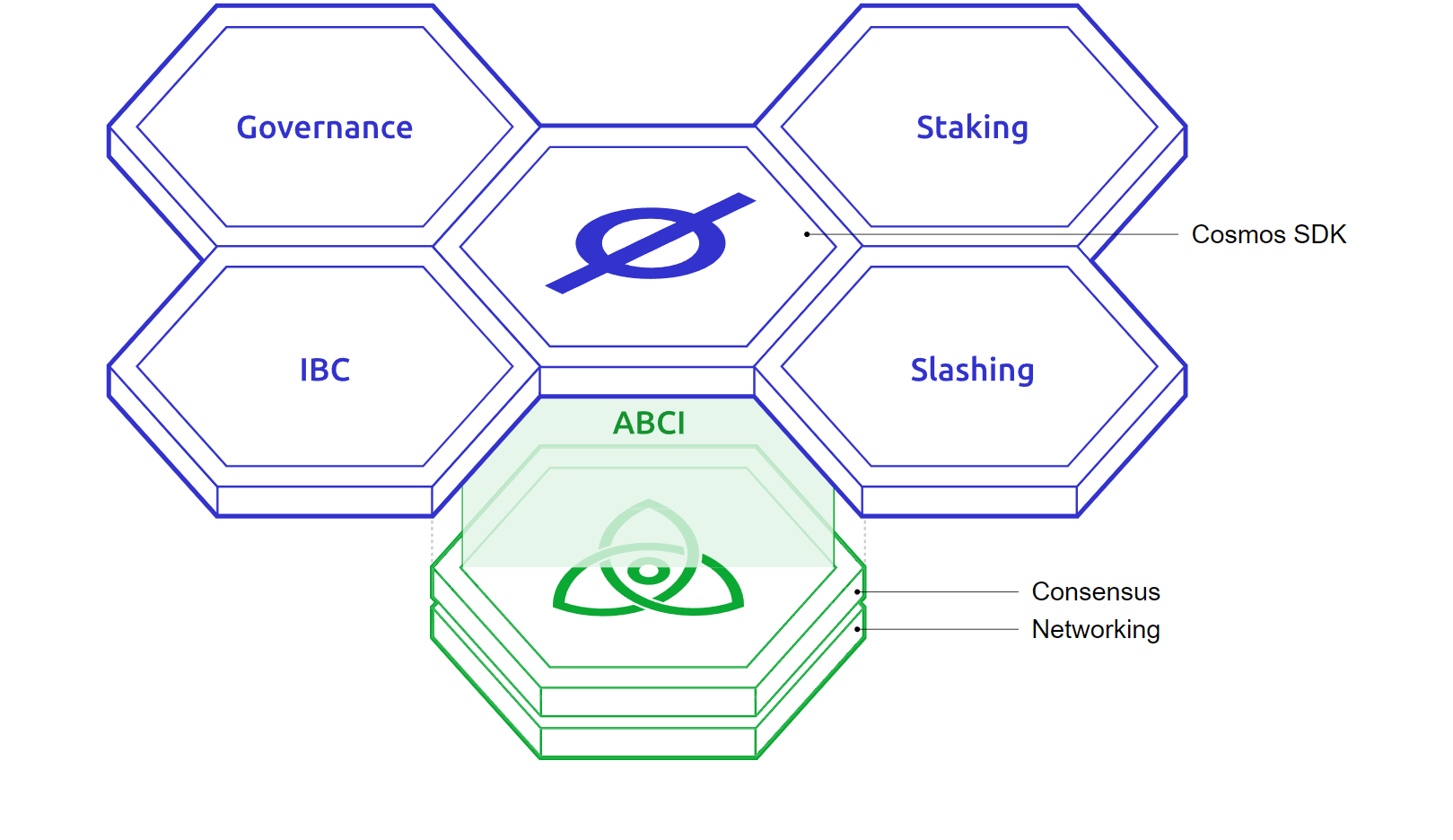

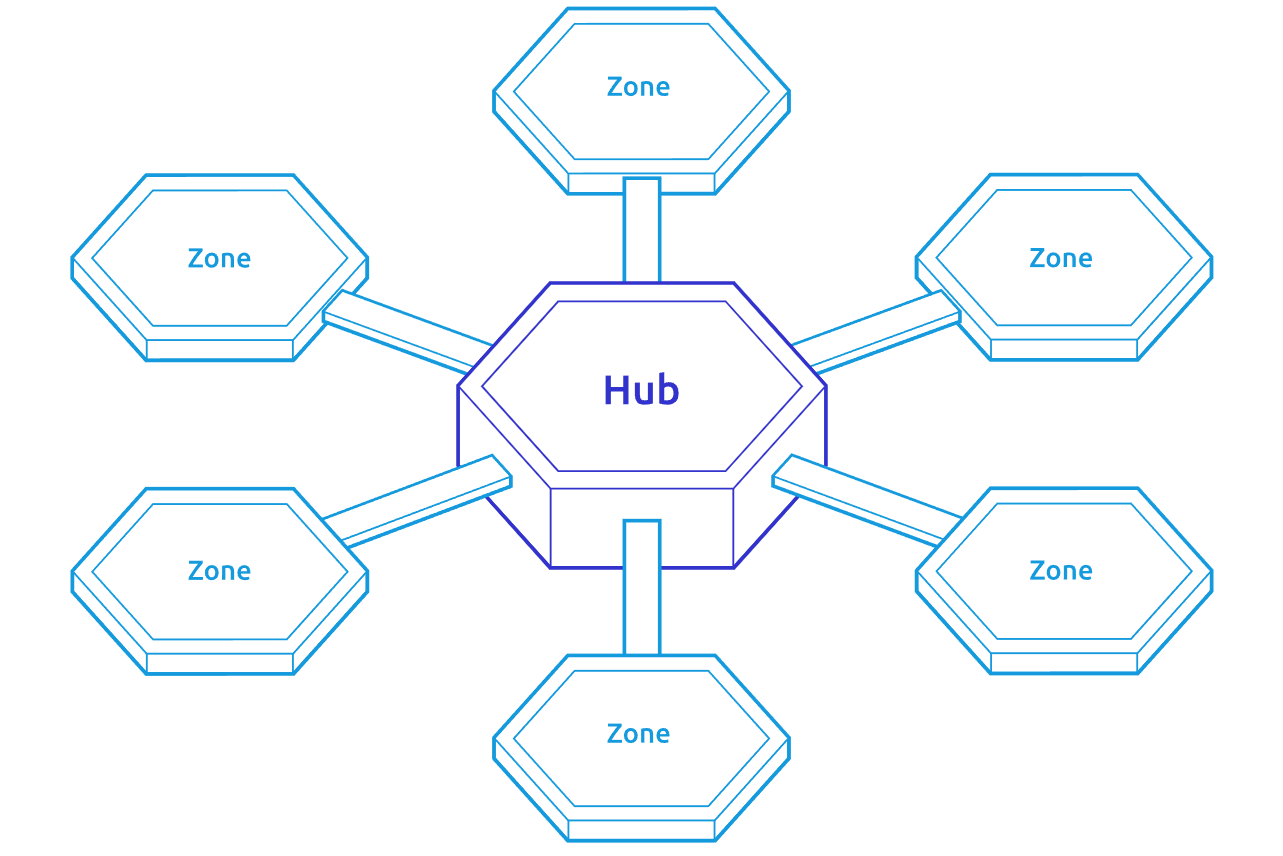

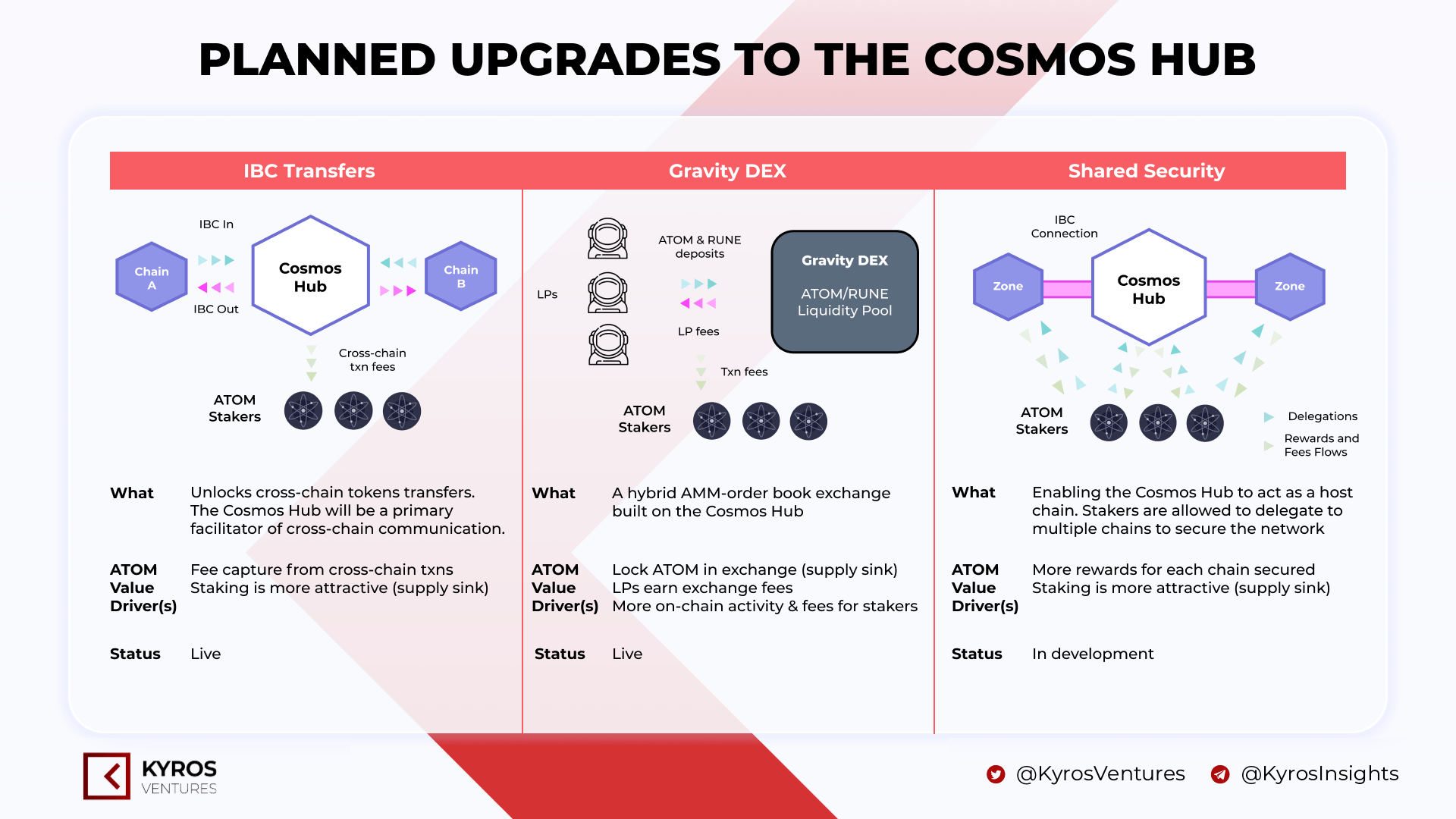

Jae Kwon first explored this continent, with the Tendermint BFT algorithm being the first seed. And from there, a Cosmos SDK development framework was formed, allowing programmers to build separate blockchains called Zones. Zones are directly connected to the Hub, the central blockchain of Cosmos, operating as a Proof-of-Stake institution. These blockchains will communicate with each other using the Inter-blockchain Communication (IBC) protocol; however, it should be noted that only blockchains with deterministic finality can use this protocol.

Some well-known countries on the Cosmos continent include Terra, Cronos, Osmosis, Evmos, or THORChain.

It is worth noting that Terra was once one of the most prosperous countries on the Cosmos continent. Terra’s native currency $LUNA has been rising continuously despite the current gloom of the blockchain world. Nonetheless, this empire collapsed within a short period, mainly due to a loophole within its framework that allows for printing the $UST stablecoin from $LUNA, leading to a death spiral when $UST was no longer pegged at $1. The Terra founding team and the community recently passed a vote to revive this country with a new domestic currency $LUNA, convert the old currency into $LUNC (Terra Classic), and $UST will forever disappear in this new sovereignty.

Other countries

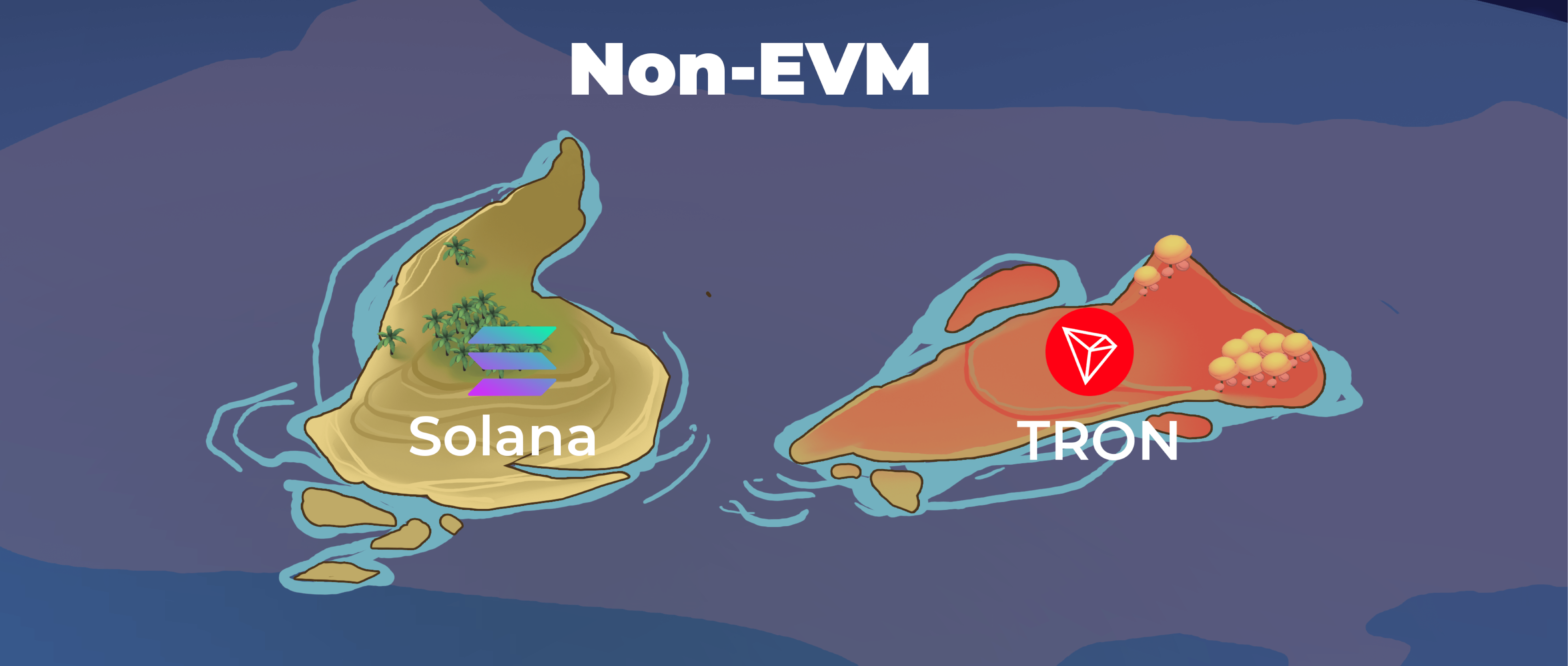

Besides these vast swathes of land, some islands are separate and not part of any Union or Commonwealth, such as Tron and Solana.

Solana

Solana is building its own empire with the current objective of being a new promising land for games and NFTs. Their strengths lie in the non-bureaucratic system, the ability to finalize transactions within milliseconds, thanks to Proof-of-History mechanism, which allows the validators to record the sequences of transactions on the network. Nevertheless, such quickness and ease-of-use in its system is a double-edged sword: there are computational bots that are designed to keep spamming the network, therefore creating unnecessary congestion or even causing a network outage, which negatively affects other citizens. In the newest proposal, the Solana team is planning to implement stake-weighting in validating transactions to mitigate this issue.

It should be noted that Solana does establish an endeavour to partner with other unions through other blockchains such as Velas, or through a smart contract such as the NEVM of Neon Labs.

TRON

Tron was founded in 2017 but appeared to be left behind compared to other nations. In June 2018, Tron declared its Independence Day and was independent from its Genesis Block. In October 2018, it established its own political philosophy, the TRON virtual machine, with a complete toolset for developers. However, because of the fixed fee of 1 USDT when transferring USDT via TRON, this country is still alive, with about 35 billion $USDT circulating in this country, even higher than the wealthiest country – Ethereum.

The most popular language: Rust

Solidity, the primary language of Ethereum, is considered the most popular language among blockchain programmers. Many blockchain platforms built later on have also used Solidity to integrate EVM and join the EVM Union to attract human resources and financial capital from this country more efficiently. However, the new concept of multi-blockchain proposed by Polkadot or Cosmos and the rise of blockchain platforms like Solana have also fueled the popularity of Rust and Golang, the two main languages spoken on those continents. Rust is now the most commonly used programming language in the blockchain world.

What’s next?

After 14 years of establishment, the blockchain world has been divided into several continents and countries with independent political philosophies or development paths. The concepts of Smart Contracts and Proof-of-Stake have unlocked up a new period of promoting economic activities and thus being applied by most countries in the blockchain world.

Besides, multi-chain activities are essential for a globalized future, promoting immigration and trade among users. But at the same time, individual blockchain nations must ensure the facets of security for their people. EVM, Polkadot and Cosmos are all potential continents towards globalization. In addition, many new initiatives will be launched to further enrich these ecosystems, thereby strengthening the overall development of the blockchain world.

Decentralization, scalability, and security have ever since challenged the idea of an open, decentralized network due to the problems of the first-generation blockchain Layer 1 Bitcoin, Ethereum, and their variants. While we’ve yet to see the upgrade of Ethereum 2.0, a new-gen Smart Contract Platform like Cosmos, Polkadot, Avalanche and LayerZero with promising proposes for the Internet of Blockchain. The term Internet of Blockchain refers to application-specific blockchains that co-exist and interoperate with one another. With several multiple-chain networks under development, it’s no certainty to forecast the winner of the scalability race between Smart Contract Platform. However, it is possible to dig deeper and explore the fundamental ideas underlying each one.

Cosmos, Polkadot, Avalanche and LayerZero have critical distinctions at the protocol level (e.g., consensus method, economic security topology) that affect platform capabilities (e.g., inter-chain communications, token economics, types of viable applications) and how they grow their networks (e.g., validator participation, staking attributions). This article aims to differences between these architectures and their trade-offs.

GETTING STARTED

To help our readers understand this topic of The Internet of Blockchain comprehensively, before diving into this topic of The Internet of Blockchain, we will walk you through a few jargons which will be used frequently in this article.

Trilemma of blockchain

A blockchain cannot possess all three attributes of scalability, decentralisation, and security.

Scalability refers to the ability of a blockchain to expand in the increased number of transactions and nodes

Decentralisation ensures that the decisions made in the network are not concentrated on one central entity